Imagine Sarah, a UK investor in Manchester, spending her Sunday manually reconciling dividend income across her ISA, SIPP, and taxable account, dreading the Capital Gains Tax calculation come January. This tedious, error-prone process isn't just frustrating; it risks costly HMRC penalties for misreporting or missing valuable allowances. As UK tax rules and pension/ISA regulations evolve, the administrative burden intensifies. So, what defines the Best Sharesight Alternative for UK Investors in 2026? This article reveals why the winner won't just track performance, but will fundamentally transform compliance. We'll show how the top contenders automate complex UK tax reporting and ISA/SIPP management, turning regulatory hurdles into seamless, integrated platform functions. Discover which tools prevent expensive mistakes and save you hours, starting today.

What Exactly is a Sharesight Alternative? (And Why UK Investors Need One in 2026)

That familiar knot in your stomach as the tax deadline looms? The frantic scramble to gather dividend statements, calculate capital gains across multiple brokers, and decipher ISA or pension contributions? For UK investors managing diverse portfolios, tax season often feels less like investing and more like an administrative nightmare. This is where portfolio trackers like Sharesight step in-but as we look towards 2026, the definition of a truly effective Sharesight alternative is undergoing a fundamental shift.

At its core, a Sharesight alternative is any portfolio tracking software designed to monitor your holdings across different brokers and accounts. It provides a consolidated view of your investments, calculates performance metrics (like your overall return), and crucially, assists with tax reporting. Traditionally, the focus was on comprehensive asset tracking-ensuring stocks, ETFs, funds, and increasingly, alternative assets or even property holdings, are all visible in one place. However, for UK investors navigating the complexities of 2026, the critical differentiator won't just be seeing your portfolio, but how smoothly the platform handles the UK's unique and evolving financial regulations.

So, why actively seek a Sharesight alternative? While Sharesight is a popular choice, UK investors often encounter specific limitations:

- UK-Specific Compliance Gaps: Sharesight's roots are in Australia, and while it offers UK tax features, its depth of integration with the intricacies of UK tax wrappers (like ISAs and SIPPs) and evolving HMRC reporting requirements can sometimes lag behind. Automating complex UK capital gains calculations, especially with upcoming changes like the Consumer Composite Investments (CCI) regime, requires deep, native understanding.

- Cost Considerations: For investors with simpler portfolios or specific budget constraints, Sharesight's pricing model might not be the most cost-effective solution, especially when premium features like advanced tax reporting are needed.

- Niche Requirements: Investors with significant holdings in specific asset classes (e.g., complex funds, private equity, crypto) or those needing highly specialised performance analysis tools (like those exploring Markowitz Portfolio Optimisation principles) might find more tailored solutions elsewhere.

The market offers significant choice-research indicates over 208 active competitors globally. Some, like MProfit (highly rated with 94.9% of users recommending it), demonstrate the demand for reliable alternatives. But in 2026, the essential reason UK investors need a capable alternative boils down to regulatory automation. It's no longer sufficient for software to just report your gains; the best platforms will transform tax calculations and ISA/SIPP management from a burdensome reporting task into an automated, core function. This means:

- Automatically applying UK tax rules (like Bed & Breakfasting, same-day rules, and the upcoming CCI reporting).

- Smoothly segregating and reporting gains/losses within tax wrappers (ISAs, SIPPs) versus taxable accounts.

- Ensuring reliable data privacy with enterprise-grade security (like end-to-end encryption) for your sensitive financial data.

- Providing clear audit trails essential for HMRC compliance.

Choosing the right Sharesight alternative in 2026 isn't just about finding a different dashboard or a cheaper price. It's about selecting a platform that acts as your automated compliance partner, deeply integrated with the UK's regulatory infrastructure. This frees you from administrative headaches, allowing you to focus on strategy-whether that's using an Investment Calculator to plan contributions, understanding risk-adjusted returns via the Sharpe Ratio, or using a Compound Interest Calculator to project long-term growth. As regulations evolve, having a tool purpose-built for the UK landscape isn't just convenient; it's becoming essential for efficient and compliant investing. Platforms like ARIA PM are emerging with this deep UK regulatory integration as their core focus, aiming to turn compliance from a chore into a seamless background process.

Why Regulatory Integration Is the REAL Differentiator for UK Investors

Let's be clear: superior portfolio analytics are now table stakes. Any credible sharesight alternative in 2026 will offer crisp performance charts, dividend tracking, and risk metrics. The true differentiator? How deeply the platform integrates with the UK's evolving regulatory infrastructure. The winner won't just report your data-it will automate your compliance, transforming tax and pension management from a manual chore into a seamless core function of the platform.

By 2026, three regulatory shifts will dominate UK investing:

- The Consumer Composite Investments (CCI) regime, tightening disclosure standards for retail investment products.

- The Public Offer Platform (POP) regime, governing how non-listed securities are offered to UK retail investors.

- HMRC reporting requirements, demanding near-real-time data on capital gains, dividends, and pension/ISA activity.

These changes amplify existing pain points. Manually calculating Capital Gains Tax (CGT) across multiple brokers is error-prone, especially with bed-and-breakfasting rules. Tracking ISA allowances or reconciling pension contributions against annual £60,000 limit often involves spreadsheets and guesswork. One missed dividend or miscalculated gain can trigger HMRC penalties.

Traditional trackers operate retrospectively-you react to problems. Next-gen alternatives bake compliance into their DNA. Imagine a platform that:

- Auto-calculates CGT liabilities as you trade, using HMRC's share-matching rules.

- Tracks your ISA allowance in real-time, alerting you before over-subscribing.

- Integrates pension contribution data directly from providers like Vanguard or Hargreaves Lansdown.

This isn't futuristic speculation. Platforms like Capitally already prioritise regulatory safety with end-to-end encryption for data privacy-a non-negotiable as cyber threats grow. Their pricing (Sailor at €80/year, Navigator at €130/year) reflects this compliance-first focus.

Your tracker should act as a compliance co-pilot. While tools like our Investment Calculator help model returns, and concepts like the Sharpe Ratio refine risk assessment, regulatory integration ensures these insights translate into actionable, audit-proof decisions. For complex portfolio construction, understanding Markowitz optimisation matters-but only if your platform automates the compliance overhead of rebalancing across taxable and tax-sheltered accounts.

In 2026, the best sharesight alternative won't just show you your returns. It will actively navigate the regulatory maze, turning compliance from a year-end nightmare into a silent, always-on safeguard. That’s the real revolution.

(ARIA PM handles survivorship adjustment, cost modelling, and regime stress-testing automatically, so you can focus on interpreting results rather than building the simulation.)

Step-by-Step: How Modern Alternatives Automate Your UK Tax and ISA Management

Forget manually updating spreadsheets every time you trade. The best Sharesight alternatives in 2026 transform UK tax and ISA management from a time-consuming chore into a seamless, automated process. Here’s how they handle the heavy lifting:

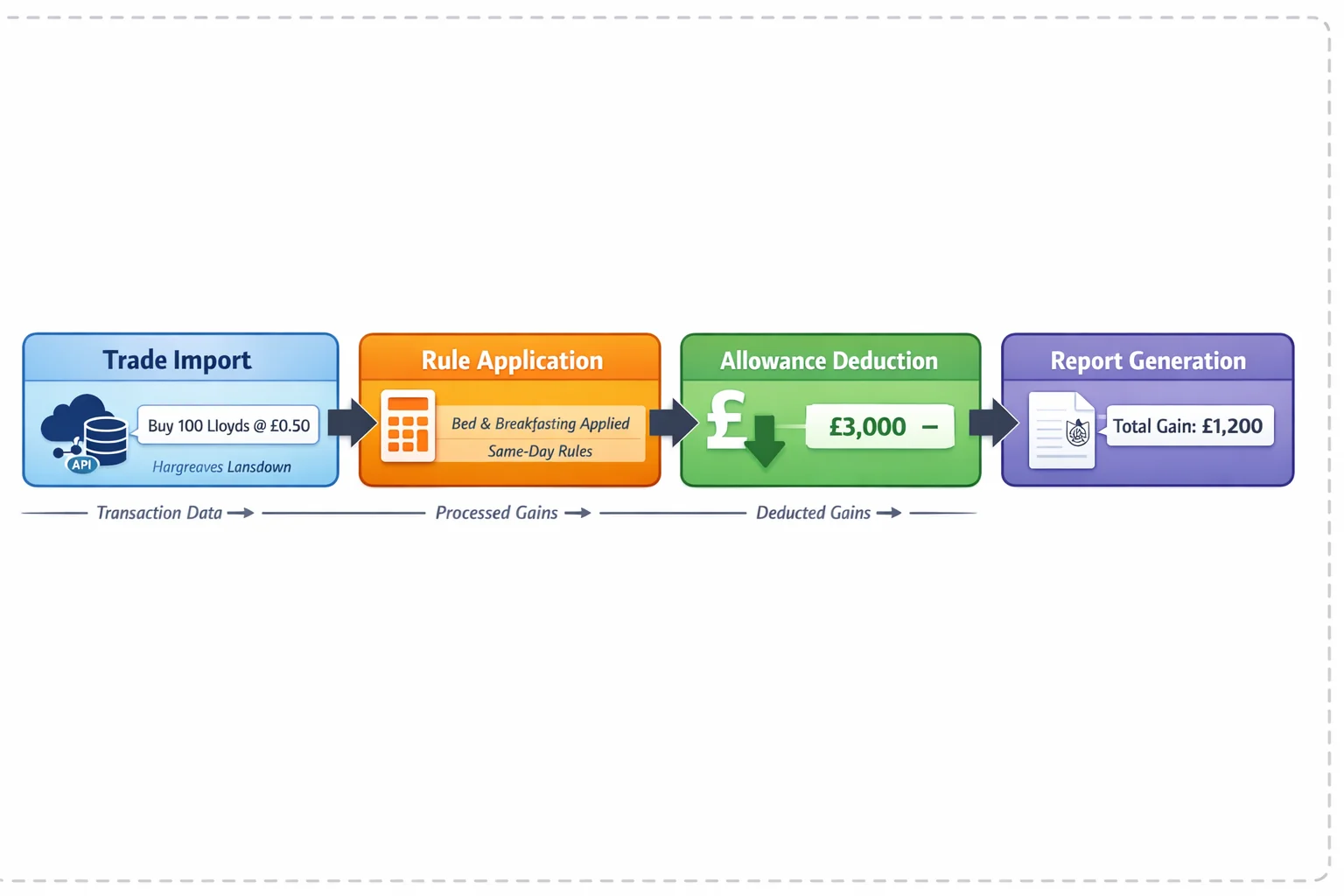

Broker Integration: Auto-Importing UK Trades Platforms connect directly to your UK brokerage accounts (e.g., Hargreaves Lansdown, Interactive Investor) and import transactions instantly. No more typing in each buy/sell. For example, sell 100 Lloyds shares at £0.50? The system logs it automatically. With over 2,000 European bank integrations (as seen in tools like Portfellow), even niche brokers are covered. This eliminates hours of spreadsheet entry and reduces errors-crucial when calculating gains for HMRC.

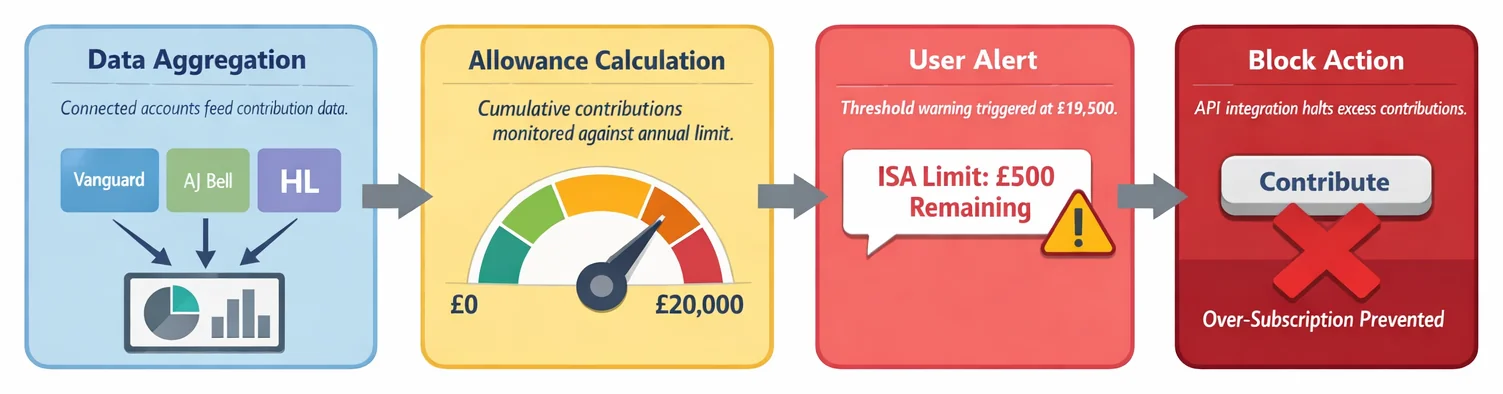

Real-Time ISA/Pension Monitoring: Flagging Allowance Breaches Your Stocks and Shares ISA or SIPP allowances are tracked live. If you contribute £19,500 by October, the tool alerts you: "ISA limit: £500 remaining." Breach the £20,000 cap? An instant notification prevents accidental penalties. For pensions, it monitors the £60,000 annual allowance, including carry-forward rules. This proactive guardrail replaces frantic year-end reconciliations.

Tax-Year Reporting: Auto-Generating HMRC-Ready CGT Reports Capital Gains Tax calculations happen in the background. When you sell assets, the platform factors in costs, allowances (£6,000 in 2023/24, reducing to £3,000 by 2024), and bed and breakfasting rules. At tax year-end, it auto-fills your Self-Assessment CGT pages with HMRC’s required format. Imagine exporting a PDF and uploading it directly-no manual sums or form wrestling.

Dividend Tracking: Categorising UK vs. International Income Dividends are automatically tagged by origin. UK dividends (like those from BP or Shell) are flagged for your £500 tax-free allowance. US or EU dividends? The system notes foreign tax credits and adjusts your liability. A £500 dividend from Unilever shows as "UK"; a €200 payment from ASML is "Netherlands-15% tax withheld." This ensures you claim the right reliefs without forensic accounting.

Beyond stocks, top platforms support alternative assets like cryptocurrency or property. Track Bitcoin gains alongside your ISA, with automated tax categorisation. And if you hit a snag, customer support resolves issues fast-vital during January’s Self-Assessment crunch.

In a market with 208 competitors (18 funded, 11 exited as of March 2026), this regulatory automation is the true differentiator. While tools like our Investment Calculator help model returns, the real win is reclaiming time. For advanced analysis-like stress-testing portfolios under different tax regimes-ARIA PM handles survivorship adjustment and cost modelling automatically. Paired with resources like our guide to the Sharpe Ratio, you spend less on compliance and more on strategy.

2026's Top Contenders Compared: Beyond Sharesight

For UK investors, the landscape in 2026 demands more than sleek charts or dividend trackers. The Public Offer Platform (POP) Regime, effective January 2026, reshapes capital-raising rules for private companies (offers over £5 million), intensifying compliance complexity. This makes deep UK regulatory integration, not analytics, the decisive factor. Here’s how top alternatives stack up:

Holistic Platforms: Security vs. Flexibility

- Capitally (€80/year) leads with on-device encryption, where data is encrypted locally before syncing to the cloud. Its automation handles HMRC tax calculations and capital gains reports smoothly, ideal for privacy-focused investors. However, it lacks dedicated ISA/SIPP tools.

- Kubera excels with alternative asset tracking (property, crypto, collectibles) but offers minimal UK tax tailoring. Its US-centric design struggles with ISA annual allowance tracking or dividend tax credits.

ISA/Pension Specialists: Family Focus

- Portfellow dominates here, automating multi-generational ISA management. It syncs with UK/EU banks to track contribution limits across Junior ISAs, SIPPs, and LISAs in real-time. Unique "family sharing" lets households pool reporting, crucial for inheritance tax planning. Yet, its analytics are basic; you’d need tools like our Sharpe Ratio Explained guide for deeper risk assessment.

Analytics-Focused: Power Without Pragmatism

- Koyfin (G2: 4.8 stars) wows with intuitive dashboards and free global data, perfect for modelling FTSE 100 scenarios. But its UK tax features are bolt-ons, ignoring POP compliance.

- Morningstar Direct (G2: 4.0 stars) offers institutional-grade data but is priced for institutions and requires manual SIPP input. For cost-efficient growth projections, our Compound Interest Calculator simplifies what Morningstar overcomplicates.

Free Tiers & Gaps

MProfit’s free tier (for smaller portfolios) suits starters but omits pension links. Capitally’s encryption is unmatched, yet its SIPP gap persists. Meanwhile, Koyfin’s lack of auto-populated HMRC reports forces manual work, a dealbreaker as POP rules evolve.

The Verdict

No platform is perfect, but Portfellow’s ISA/pension automation and Capitally’s compliance-driven encryption lead for 2026. For investors prioritising growth strategy alongside compliance, tools like our Investment Calculator or Markowitz Portfolio Optimisation guide fill analytics gaps. Remember: the winner isn’t the smartest tool, but the one that turns regulatory headaches into background processes.

(Need to stress-test your strategy under POP rules? ARIA PM handles regime shifts automatically, so you focus on decisions, not data entry.)

Costly Mistakes UK Investors Make When Choosing a Tracker

Selecting the wrong portfolio tracker in 2026 could cost you thousands in penalties or hundreds of wasted hours. As regulatory complexity grows, UK investors often stumble into these traps:

Mistake 1: Prioritising flashy analytics over HMRC compliance tools Many platforms dazzle with heatmaps and predictive algorithms while neglecting core UK tax functions. The consequence? You’ll spend weekends manually reconciling dividends or calculating capital gains. Imagine cross-referencing 200+ transactions across ISAs, SIPPs, and taxable accounts-a real risk if your tracker lacks automated HMRC-compliant tax reporting. Fix: Demand sample Capital Gains Tax and dividend reports before subscribing. Verify they match HMRC’s required formats.

Mistake 2: Ignoring military-grade data security With investment platforms handling your entire financial footprint, lax security is catastrophic. Unlike basic password protection, leaders like Capitally now use end-to-end encryption-the benchmark for sensitive data. Overlooking this risks exposing your holdings, personal details, and transaction history. Fix: Confirm encryption standards and multi-factor authentication are non-negotiable features.

Mistake 3: Assuming universal UK integration Not all platforms sync with UK brokers or pension providers. If your tracker can’t connect to your AJ Bell SIPP or Hargreaves Lansdown ISA via direct bank APIs, you’re stuck with error-prone CSV uploads. Worse, the new Consumer Composite Investments (CCI) regime-replacing PRIIPs/UCITS-demands real-time product summary updates many trackers ignore. Fix: Test integrations with your actual accounts during free trials. Ensure CCI documentation is auto-synced.

Mistake 4: Underestimating ISA allowance complexity Manually tracking your £20,000 annual ISA allowance across multiple providers invites over-contribution fines. Few trackers automate this, and fewer still handle Bed & ISA transfers (selling shares in a taxable account and rebuying within an ISA). One missed transfer could trigger unnecessary CGT bills. Fix: Verify real-time ISA allowance tracking and Bed & ISA automation. Use our Investment Calculator to model tax savings from efficient transfers.

With 18+ funded competitors innovating rapidly, 2023’s "adequate" tracker is 2026’s liability. Platforms like ARIA PM now treat UK tax and pension compliance as core functions-not bolt-ons-automating everything from CCI regime updates to SIPP contribution tracking. Before choosing, prioritise these safeguards over glossy analytics. Your future self will thank you when tax season arrives.

Pro tip: Test drive tools using our Free Tools suite to gauge usability, and explore how automated compliance impacts long-term returns via our ROI Calculator.

Your 30-Minute Action Plan: Finding Your Ideal 2026 Tracker

Stop dreading tax season. The right Sharesight alternative won’t just track returns, it’ll automate UK tax compliance and pension management, turning regulatory headaches into background processes. Here’s how to find your match in 30 minutes:

1. Audit Your Needs (5 mins) List every broker, ISA (Stocks & Shares, Lifetime), and pension (SIPP, workplace) you use. Why? Platforms like Capitally sync with HMRC’s real-time systems, but only if they support your providers. Include niche holdings like Public Offer Platform (POP) regime shares, these £5M+ capital-raising instruments require specific tax treatment.

2. Test 3 Platforms (15 mins) Prioritise free trials:

- Capitally (14-day trial): Ideal if privacy is non-negotiable.

- MProfit (free tier): Strong for multi-currency pensions.

- Portfellow: Best for SIPP automation. Import one brokerage account to each. Check dashboards for clarity, can you instantly see ISA vs. taxable holdings?

3. Validate UK Features (5 mins) Ask support: "Show me a sample CGT report for UK assets." Watch for:

- Automatic Bed and Breakfasting rule application.

- Dividend tax calculations aligning with HMRC’s 2026 thresholds.

- Goal-based portfolio strategy tools (e.g., "Retire at 60" projections). If a platform can’t simulate how new POP investments affect your goals, skip it.

4. Security Check (5 mins) Confirm end-to-end encryption and UK data centres. Avoid platforms storing data under lax regimes (e.g., non-FCA jurisdictions).

G2 ratings (like Koyfin’s 4.8) signal usability, but UK-fit is critical. For advanced modelling, like survivorship bias adjustment or regime stress-testing, tools like ARIA PM automate this, freeing you to interpret results.

Start Tonight: This saves 10+ hours/year on tax prep. Use reclaimed time to optimise returns:

- Model compounding gains with our Investment Calculator (£10K at 7%/yr = £19,672 in 10 years).

- Refine allocations using Markowitz principles.

- Measure efficiency via the Sharpe Ratio.

Your move: Test one platform now. Your future self will thank you.

Explore more resources in our Free Tools hub, or calculate your potential savings with our ROI Calculator.

![]()

Key Takeaways

- Prioritise platforms that automate UK tax calculations and wrapper management (ISAs/SIPPs) over those merely offering portfolio analytics.

- Verify the platform produces HMRC-ready capital gains data compatible with Self Assessment (SA108) and the real-time CGT reporting requirements where they apply.

- Ensure the solution smoothly tracks ISA and SIPP contributions/withdrawals for accurate annual allowance monitoring.

- Assess if the platform's cost reflects your portfolio complexity, especially if UK-specific automation replaces expensive manual tax work.

| Task | Traditional Manual Approach | Modern Automated Approach (2026) |

|---|---|---|

| Dividend Income Tracking | Collect statements from multiple brokers, reconcile in spreadsheets | Automatically aggregates dividends across all linked accounts, categorises by tax status |

| Capital Gains Calculation | Manually calculate gains/losses per trade using HMRC rules | Real-time CGT liability tracking with automatic same-day/30-day rule application |

| ISA/SIPP Contribution Monitoring | Track allowances via spreadsheets or memory | Live allowance tracking with alerts at 80%/100% thresholds |

| Tax Reporting (Self Assessment) | Compile data manually for SA108 forms | Generates pre-filled HMRC-compliant tax reports for direct submission |

| POP Regime Compliance | Manual documentation for private company offers | Auto-flags investments subject to £5M+ capital raises, provides compliance templates |

Critical Tracker Selection Criteria for UK Investors (2026)

| Feature | Basic Trackers | Advanced UK-Optimised Platforms | Why It Matters in 2026 |

|---|---|---|---|

| HMRC Rule Integration | Limited or generic tax logic | Deeply embedded UK CGT/dividend rules | Ensures accurate tax calculations as regulations evolve |

| ISA/SIPP Automation | Manual allowance tracking | Real-time contribution monitoring with HMRC alerts | Prevents over-contribution penalties (£6k+ potential fines) |

| POP Regime Support | None | Automated compliance flagging + reporting | Essential for private company investors post-January 2026 |

| Broker Integration Depth | Partial UK broker coverage | Full FCA-regulated broker API links | Eliminates manual entry errors for trades/dividends |

| Security & Audit Compliance | Basic encryption | FCA-grade security + tamper-proof logs | Meets FCA data protection requirements for financial tools |

Sources

- FCA: Investment Platforms Market Study, FCA's analysis of platform services, features and consumer considerations for UK investors.

- Investopedia: Portfolio Management Tools, Comparative reviews of portfolio trackers, updated regularly for global and UK-specific options.

- Bogleheads: Tools and Calculators, Community-vetted resource listing portfolio trackers with UK tax compliance features.

- Which? Investment Platform Reviews, Independent comparisons of UK platforms' tracking features, fees and usability.

- MoneySavingExpert: Cheap Share Dealing, Authoritative UK guide evaluating platforms' portfolio tracking capabilities and costs.

- SEC: Investor Bulletin: Automated Investment Tools, Regulatory guidance on key features and risks of portfolio management technology.