This article cuts through the complexity to answer that question using Markowitz Portfolio Optimisation. Forget chasing the hottest stocks; Markowitz reveals the real secret lies in how assets move together. We'll show you why adding certain volatile assets can lower your overall risk more effectively than just piling into low-risk options alone-a powerful "diversification multiplier" effect. You'll learn practical, jargon-free strategies to build a resilient portfolio suited to UK markets, avoid common costly mistakes, and get a clear 30-day action plan-no prior expertise needed.

What Markowitz Portfolio Optimization Really Means (And Why It's Not Stock-Picking)

We’ve all been tempted: a friend brags about a "sure-fire" stock, headlines scream about soaring tech shares, and suddenly you’re imagining life-changing gains. But chasing individual winners rarely ends well. Why? Because even the hottest stock can crash overnight, leaving your portfolio exposed. This is where Markowitz Portfolio Optimisation (MVO) flips the script entirely. It’s not about stock-picking at all, it’s a mathematical strategy that engineers safety through smart combinations.

Developed by Nobel laureate Harry Markowitz in 1952, MVO solves a counterintuitive puzzle: how adding volatile assets can actually reduce your overall risk. The secret lies in covariance, a measure of how investments move relative to each other. If one asset zigs when another zags (like UK stocks and government bonds), their negative correlation acts as a shock absorber. MVO exploits this to build portfolios where risk isn’t just averaged, it’s strategically cancelled out.

The "Diversification Multiplier" in Action

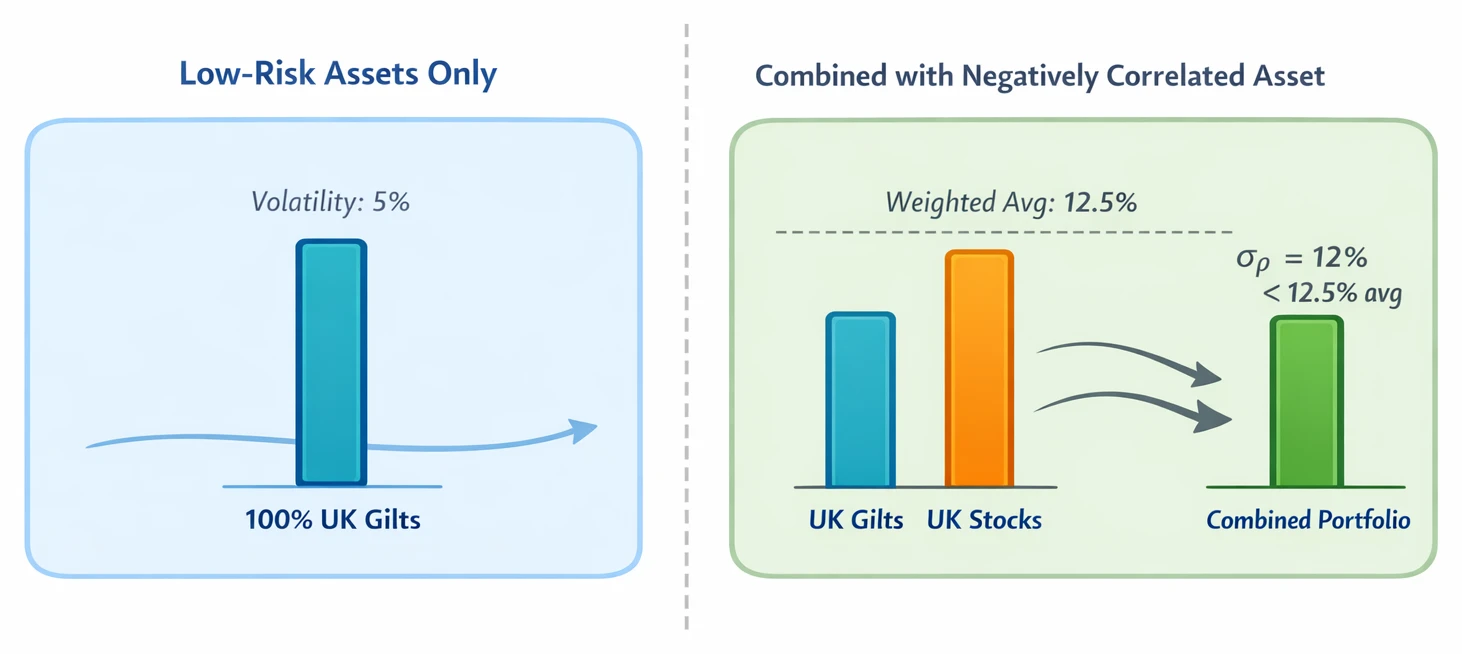

Imagine you hold only UK gilts (government bonds). They’re stable but offer modest returns. Now add FTSE 100 stocks. Individually, stocks are riskier, they swing wildly with economic news. But historically, when stocks fall, gilts often rise as investors flee to safety. MVO mathematically combines them so the portfolio’s combined volatility drops below the average of the two. This is the "diversification multiplier": by prioritising assets that don’t move in lockstep, you get smoother returns than holding low-risk assets alone.

Contrast this with the "high-return obsession." Suppose you pick two FTSE stocks like BP and Shell. Both might soar when oil prices rise, but they’ll also crash together during an energy slump. MVO would flag this redundancy, their positive covariance offers little risk reduction. Instead, it might pair BP with a negatively correlated asset like renewable energy stocks or inflation-linked gilts, engineering stability no single "winner" can provide.

Why Markowitz Still Dominates Finance

Markowitz’s 1952 paper remains astonishingly relevant, accumulating over 70,000 academic citations and gaining 2,000-3,000 new citations yearly. Modern research turbocharges his framework: roughly 25%-35% of new studies focus on "reliable" MVO (which handles market uncertainty), while 20%-30% blend it with machine learning to predict asset behaviour. Annual publications on portfolio optimisation grow at 8%-12%, proof that MVO’s core insight is timeless: true optimisation isn’t about picking stars, but choreographing how assets dance together.

In short, MVO isn’t a crystal ball for hot stocks. It’s a blueprint for building portfolios where risk isn’t avoided, it’s engineered into silence.

The Diversification Multiplier: Why Covariance Beats Low-Risk Assets

Imagine building a portfolio like assembling a puzzle. The individual pieces (assets) might look jagged and risky alone, but when you find ones that fit together smoothly, the whole picture becomes stable and clear. That's the diversification multiplier in action. Harry Markowitz's breakthrough wasn't about hunting for the "best" assets. It revealed that combining volatile assets which zig when others zag-thanks to negative covariance-can actually reduce your overall risk more than simply stuffing your portfolio with low-risk assets alone.

Think of it like this: UK tech stocks might surge 15% one year but crash 20% the next. UK government bonds (gilts), however, often rise when stocks panic, as investors flee to safety. If you hold both, the bonds act like shock absorbers. When tech stocks tumble, your gilts likely gain, cushioning the blow. This negative correlation means the combined portfolio dances to a calmer tune than either asset solo. Paradoxically, adding a "risky" tech stock to a gilt-heavy portfolio can lower your overall volatility because of this offsetting effect.

This insight is so powerful that 60-80% of institutional investors use Markowitz optimisation as their foundation for strategic asset allocation. But here's the catch: to build this puzzle, you need precise measurements of how every asset interacts. For just 100 assets, you must estimate 100 expected returns, 100 variances, and a staggering 4,950 covariances (totalling 5,150 parameters!). Get one wrong-like overestimating how tightly tech stocks and gilts move together-and your "optimal" portfolio can become dangerously unstable.

That's why over 80% of professionals impose weight limits (e.g., capping tech stocks at 15%) and 40-60% use shrinkage estimators-statistical tools that blend historical data with conservative assumptions to tame wild predictions. Innovations are helping: over 30% of new research papers now combine Markowitz with machine learning to handle these parameter mountains.

The lesson? True diversification isn't just owning many assets. It's engineering a collaboration where volatility cancels out, letting you achieve smoother returns than low-risk assets could ever deliver alone. It’s the hidden multiplier that turns risk into resilience.

A Step-by-Step Walkthrough (Without the Math)

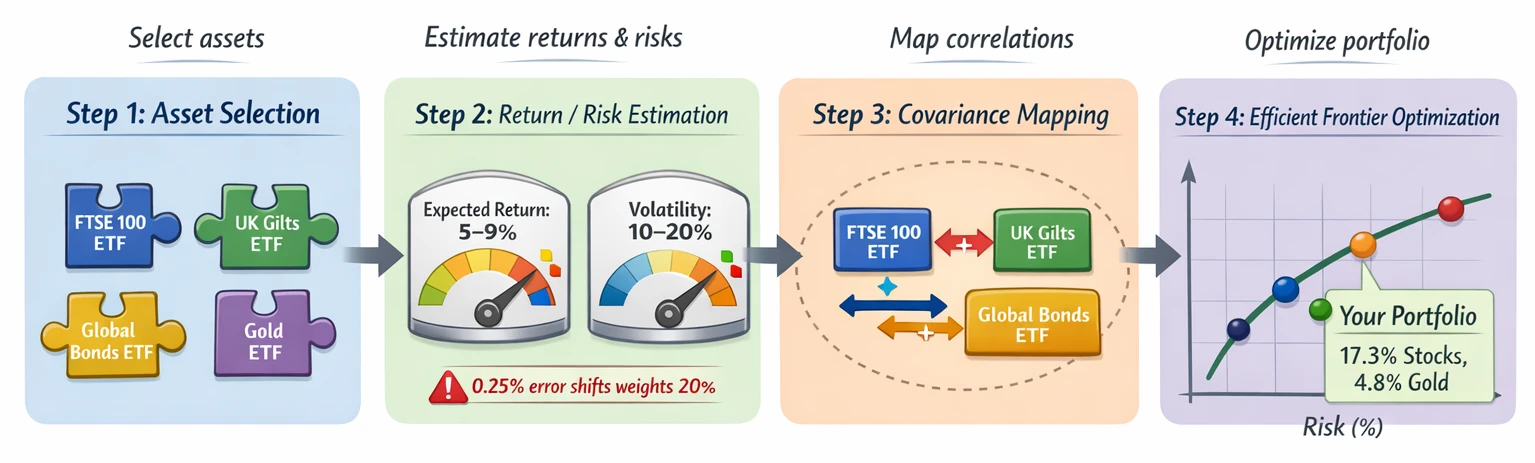

Step 1: Pick Your Building Blocks Start by choosing a basket of assets, like ETFs tracking the FTSE 100, gold, government bonds, or global stocks. Think of these as ingredients for a recipe. The goal isn’t to find the single "best" performer. Instead, you’re gathering pieces that different jobs in your portfolio. For example, bonds often stabilise stocks during market crashes, while gold might surge when inflation spikes.

Step 2: Guesstimate Future Returns and Risks Next, estimate two things for each asset:

- Expected return: How much profit you think it might deliver annually (e.g., 7% for stocks, 3% for bonds).

- Risk: How wildly its value might swing (measured as volatility).

Here’s the catch: tiny errors matter. If you misjudge an asset’s return by just 0.25-0.50% (25-50 basis points), the "optimal" portfolio can shift dramatically, like swapping a 20% allocation in stocks for bonds overnight. Returns are notoriously hard to predict, making this the shakiest step.

Step 3: Map How Assets Move Together (The "Shock Absorber" Effect) This is Markowitz’s masterstroke. Instead of viewing assets in isolation, measure their covariance, how they interact. Imagine:

- Stocks and bonds often move in opposite directions (negative covariance). When stocks crash, bonds might rally, acting like "financial shock absorbers."

- Two tech stocks might surge and plunge together (positive covariance), doubling your risk.

The magic? Adding a volatile asset (like crypto) that zigs when others zag can lower your overall risk more than stuffing your portfolio with "safe" assets alone. But beware: estimating these relationships requires mountains of data. For 100 assets, you’d ideally need 300-1,000 data points. Yet 10 years of monthly prices only gives 120, making covariance guesses prone to error.

Step 4: Find Your "Sweet Spot" on the Menu Plug your estimates into an optimiser. It scans millions of combinations to build the efficient frontier, a curve plotting the highest possible return for every level of risk. Think of it as a "risk-return menu":

- Low-risk options (left side): Heavy on bonds, lower returns.

- High-risk options (right side): Stock-heavy, potentially higher rewards.

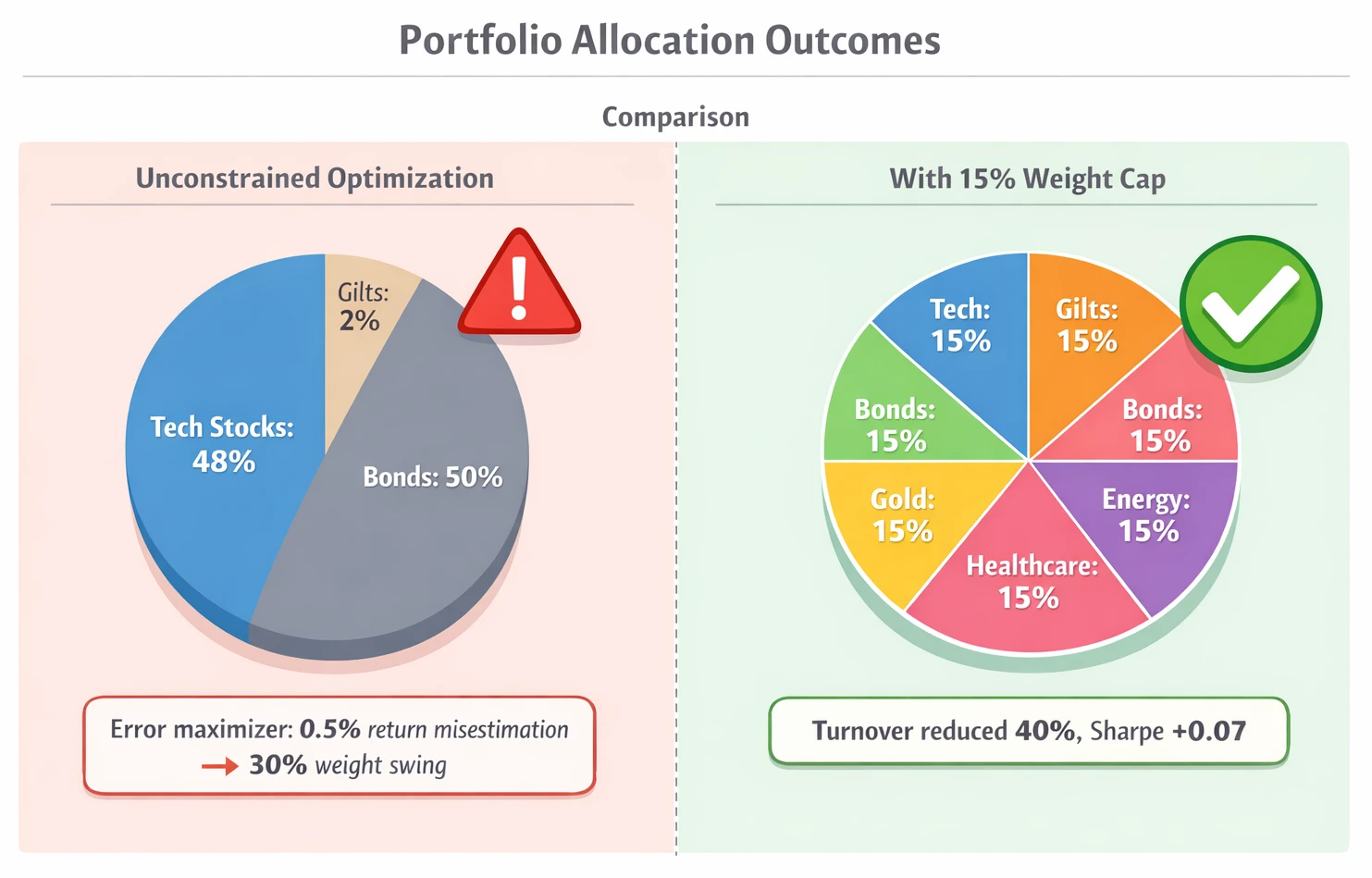

The optimiser picks your "optimal" portfolio along this curve, spitting out precise weights like "17.3% in stocks, 4.8% in gold." This precision is seductive but deceptive, it treats rough estimates as gospel. In reality, over 80% of professionals add guardrails, like capping single assets at 10% or banning negative weights (short-selling). Why? Unconstrained portfolios often recommend extreme bets (e.g., 50% in one asset) that backfire if estimates are off.

The Real-World Twist Textbook Markowitz assumes perfect foresight, but humans guess imperfectly. That’s why:

- Equal-weighted "1/N" portfolios (e.g., 25% each in 4 assets) often match or beat optimised portfolios out-of-sample.

- robust versions (using constraints or smarter estimates) lift risk-adjusted returns by 0.05-0.20 on the Sharpe ratio, a meaningful edge.

Tools like ARIA PM automate the heavy lifting, survivorship bias adjustments, cost modelling, and stress-testing across market regimes, so you focus on strategy, not spreadsheet nightmares. Remember: optimisation is a compass, not a GPS. It points toward diversification’s power, but the path demands humility about uncertainty.

Practical Tools and Strategies for UK Investors

So, how can you apply Markowitz approach without a PhD? The core idea is simple: diversification isn’t just about holding different assets, it’s about combining assets that move differently to engineer lower risk. Here’s how to put this into practice in the UK, whether you’re hands-off or DIY-inclined.

Start Simple: Pre-Built Solutions

For most investors, robo-advisors like Nutmeg or Moneyfarm are the easiest entry point. They automate Markowitz-style optimisation, using algorithms to build portfolios from ETFs based on your risk tolerance. Fees start around 0.45%-0.75% annually, reasonable for set-and-forget simplicity.

Alternatively, consider multi-asset funds like Vanguard’s LifeStrategy range. These "all-in-one" funds hold thousands of global stocks and bonds, pre-optimised for diversification. The equity/bond mix (e.g., 60% stocks/40% bonds) handles covariance for you, with fees under 0.25%.

DIY: Build Your Own Diversified Portfolio

If you prefer control, begin with 3-5 low-cost ETFs covering major asset classes. Aim for assets that historically don’t move in lockstep:

- UK equities (e.g., iShares Core FTSE 100 UCITS ETF)

- Global equities (e.g., Vanguard FTSE All-World UCITS ETF)

- UK gilts (e.g., iShares UK Gilts All Stocks ETF)

- Global bonds (e.g., Vanguard Global Aggregate Bond UCITS ETF)

Example starter portfolio (£10,000):

- 40% FTSE All-World ETF

- 30% FTSE 100 ETF

- 30% Global Bond ETF

Rebalance annually to maintain weights. Tools like Morningstar’s X-Ray help visualise your portfolio’s diversification and risk exposure for free.

Institutional Tricks to Steal

Professional investors know raw Markowitz models have flaws. Over 80% use weight constraints (e.g., capping single assets at 10-15%) to avoid extreme allocations. Why? Unconstrained optimisation can trigger 100%-300% annual turnover, meaning constant buying/selling. Transaction costs (10-50 basis points per trade) could erode £100-£500 yearly on a £100,000 portfolio. Constraints slash turnover to 20%-80%, protecting returns.

Similarly, 40%-60% of funds use covariance smoothing (shrinkage estimators) to stabilise volatility forecasts. This technique reduces realised portfolio volatility by 5%-20% and turnover by 10%-40%, while lifting risk-adjusted returns (Sharpe ratios) by 0.03-0.10.

For risk-averse investors, minimum-variance portfolios, which skip return predictions entirely, can cut volatility by 10%-25% and boost Sharpe ratios by 0.05-0.15 versus traditional approaches.

Costs & Cautions

- Fees matter. A 0.5% higher annual charge could cost you £3,461 over 20 years on a £10,000 investment (at 7% vs 6.5% growth).

- Use tax-efficient wrappers (ISAs, SIPPs) to shield gains.

- Avoid overcomplication: Start with broad asset classes. Adding niche holdings (e.g., crypto, single stocks) often increases risk without improving diversification.

Tools like ARIA PM simplify advanced optimisation, automating cost modelling, survivorship bias adjustment, and stress-testing across market regimes, so you can focus on strategy, not spreadsheet errors.

Bottom line: You don’t need complex math. Use off-the-shelf solutions or a handful of diversified ETFs, apply basic constraints, and let covariance do the heavy lifting.

5 Costly Mistakes Retail Investors Make (And How to Avoid Them)

1. Chasing Past Winners Many investors pick assets solely because they’ve performed well recently. But Markowitz optimisation relies on future returns and correlations, not historical ones. As Best and Grauer (1991) proved, even tiny errors in estimating expected returns (like 0.25%-0.50%) can wildly distort your "optimal" portfolio. Example: Loading up on tech stocks after a boom, only to suffer when correlations converge during a crash. Solution: Use long-term averages (e.g., 10+ years of data) for inputs, not last year’s stars.

2. Ignoring the "Error Maximiser" Effect Markowitz models are hypersensitive. Michaud (1989) famously called them "error maximisers" because they amplify estimation mistakes. If you inaccurately gauge an asset’s risk or correlation, the model might over-allocate to it. Example: Assigning 40% to a "low-risk" corporate bond fund that later crashes when defaults spike. Solution: Apply 5-10% weight caps per asset to limit exposure.

3. Overcomplicating With Too Many Assets Adding hundreds of assets feels diversified, but DeMiguel, Garlappi, and Uppal (2009) showed this backfires without enough data. For 100 assets, you need 300+ months of returns (25 years!) to reliably estimate correlations. Most investors lack this, leading to garbage-in-garbage-out results. Solution: Start simple. Build a reliable core with 3-5 broadly diversified assets (e.g., a global stock ETF, government bonds, and a commodity fund).

4. Blindly Trusting "Optimal" Outputs Unconstrained optimisers often suggest extreme allocations, like 90% to a niche asset. This ignores real-world constraints: liquidity, trading fees, or your own risk tolerance. Example: A model recommending 80% allocation to emerging markets because of a temporary yield spike, exposing you to currency crashes. Solution: Always impose realistic constraints (e.g., max 15% per asset) and stress-test outcomes. Tools like ARIA PM handle survivorship bias and cost modelling automatically, letting you focus on practical adjustments.

5. Rebalancing Too Often Frequent tweaking to maintain "optimal" weights triggers transaction fees and taxes on gains. If you rebalance monthly, a £100,000 portfolio growing at 7% annually could lose over £3,000 more in costs across 10 years versus annual rebalancing. Solution: Rebalance once a year or when allocations drift 5-10% from targets.

The Bottom Line Markowitz’s genius was showing diversification isn’t just hoarding low-risk assets, it’s mixing volatile, negatively correlated holdings (like stocks and gold) to reduce total risk. But without disciplined inputs and constraints, optimisation becomes guesswork. Start small, cap weights, and prioritise long-term data over short-term noise.

Your 30-Day Markowitz Action Plan

Putting Markowitz’s insights into practice doesn’t require complex maths, just disciplined steps. Here’s how to build your "diversification multiplier" in four weeks:

Week 1: Audit Your Current Portfolio Start by scrutinising your existing holdings. Many investors discover they’re accidentally overexposed to one sector (e.g., tech) or region (e.g., UK-only stocks). List every investment, shares, funds, bonds, and categorise them by asset class and geography. Ask: "Do my UK stocks all move together when the FTSE dips? Are my bonds truly balancing my equities?" Use a simple spreadsheet or free apps like Morningstar to spot overlaps. The goal isn’t perfection, but awareness.

Week 2: Select 3-5 Low-Cost ETFs Next, pick exchange-traded funds (ETFs) that cover diverse, non-correlated markets. Focus on low fees (under 0.2% annually) to avoid eroding returns. For UK investors, consider:

- Global equities (e.g., iShares Core MSCI World UCITS ETF)

- UK government bonds (e.g., iShares Core UK Gilts UCITS ETF)

- Emerging markets or commodities (e.g., iShares Core MSCI EM IMI UCITS ETF) Stick to 3-5 funds, enough for diversification, but manageable. Platforms like Vanguard or HSBC offer these.

Week 3: Check Historical Relationships Use free tools like Portfolio Visualizer to test how your chosen ETFs interacted historically. Look for negative correlation, e.g., when stocks fell, did bonds rise? If two assets often move in opposite directions (like equities and gilts during recessions), they’ll amplify your "diversification multiplier." For deeper analysis, tools like ARIA PM handle survivorship adjustment, cost modelling, and regime stress-testing automatically, letting you focus on interpreting results.

Week 4: Set Allocation, Then Step Back Assign simple weights: e.g., 60% equities, 40% bonds. Cap any single ETF at 20-25% to limit overconcentration. Crucially:

- Automate contributions via your brokerage.

- Rebalance annually, no daily tinkering.

- Hold investments in a Stocks and Shares ISA to shield gains from tax. If your situation is complex (e.g., large inheritance or nearing retirement), consult a fixed-fee advisor.

The Long Game Markowitz’s Nobel-winning insight wasn’t about chasing "hot" stocks, it proved that engineered diversification lowers risk more effectively than low-volatility assets alone. By prioritising mix over magic bullets, you harness volatility as a tool. Stay disciplined: a £10,000 portfolio growing at 7% annually for 20 years becomes £38,697. Miss just 1% due to panic-selling or fees, and it drops to £32,071, a £6,626 difference. Trust the process, and let covariance work for you.

Key Takeaways

- Markowitz optimisation proves that combining volatile assets with negative covariance (like UK shares and gilts) lowers portfolio risk more effectively than holding only low-risk assets.

- Focus on how assets move together (covariance), not just their individual returns, when building your portfolio to achieve true diversification.

- Prioritise including assets that historically move in opposite directions during market stress (e.g., shares falling while gilts rise) to act as a natural shock absorber.

- Avoid simply piling into multiple high-return assets from the same sector (like BP and Shell), as their positive covariance offers minimal risk reduction.

- Understand that adding a volatile asset can paradoxically decrease your portfolio's overall volatility if it is negatively correlated to your existing holdings.

| Approach | Core Focus | Risk Management Strategy | Key Outcome |

|---|---|---|---|

| Traditional Stock-Picking | Selecting "winning" individual assets | Holding perceived safe/low-risk assets | High vulnerability to single-asset volatility; often underperforms benchmarks |

| Markowitz Optimisation | Combining assets via covariance | Exploiting negative correlations | "Diversification multiplier" effect: Lower overall risk for target return |

Risk Reduction Strategies Compared

| Strategy | How It Works | Risk Reduction Source | Key Advantage |

|---|---|---|---|

| Low-Risk Assets Alone | Only holds stable assets (e.g., UK gilts) | Relies solely on individual stability | Predictable but limited returns; no collaboration between assets |

| Diversification Multiplier | Mixes volatile assets with negative covariance | Assets offsetting each other's swings | Achieves lower risk than low-asset approach; unlocks higher return potential |