Picture this: your Stocks and Shares ISA or SIPP surged last quarter, but now markets are swinging wildly. You feel the urge to "fix" things — sell the losers, chase the winners. Sound familiar? This emotional tug-of-war risks derailing your long-term strategy and potentially locking in losses. How Often Should You Rebalance Your Portfolio? A UK ISA and SIPP Investor's Guide tackles this core dilemma. We'll show why the best approach isn't rigid calendars or market timing, but using rebalancing as a behavioural tool. Discover how setting wider allocation bands (+/-10%) enforces disciplined buying-low and selling-high during volatility, reduces costly emotional trading, and crucially, makes use of the tax-free efficiency of your ISA and SIPP wrappers. Learn why rebalancing less often, but smarter, is often the key to staying on track.

What Portfolio Rebalancing Is and Why It Matters for Your ISA/SIPP

Imagine you started with a balanced portfolio of 60% stocks and 40% bonds in your ISA or SIPP. After a strong stock market rally, your equities surge to 70% of your portfolio while bonds shrink to 30%. Suddenly, your investments are far riskier than you intended. This drift happens naturally as markets move, and it’s why portfolio rebalancing matters. Simply put, rebalancing means adjusting your investments back to your original target allocations, like resetting that 60/40 split, by selling outperforming assets and buying underperforming ones.

Its core purpose isn’t chasing higher returns but controlling risk. Without rebalancing, you could become overexposed to volatile assets (like stocks after a bull run), leaving you vulnerable to bigger losses during downturns. For UK investors, SIPP, and ISA holders, this process is uniquely efficient. Trades within these tax-free wrappers incur no capital gains tax, making rebalancing far more cost-effective than in taxable accounts. You’re free to adjust holdings without the friction of tax penalties.

Critically, rebalancing acts as a behavioural safeguard. It forces you to "buy low and sell high" mechanically, counteracting the emotional urge to chase rising markets or panic-sell during crashes. Research has shown that disciplined rebalancing can enhance long-term returns by maintaining your intended risk profile and capitalising on market volatility. Tools like our Portfolio Calculator help visualise these drifts and simulate adjustments.

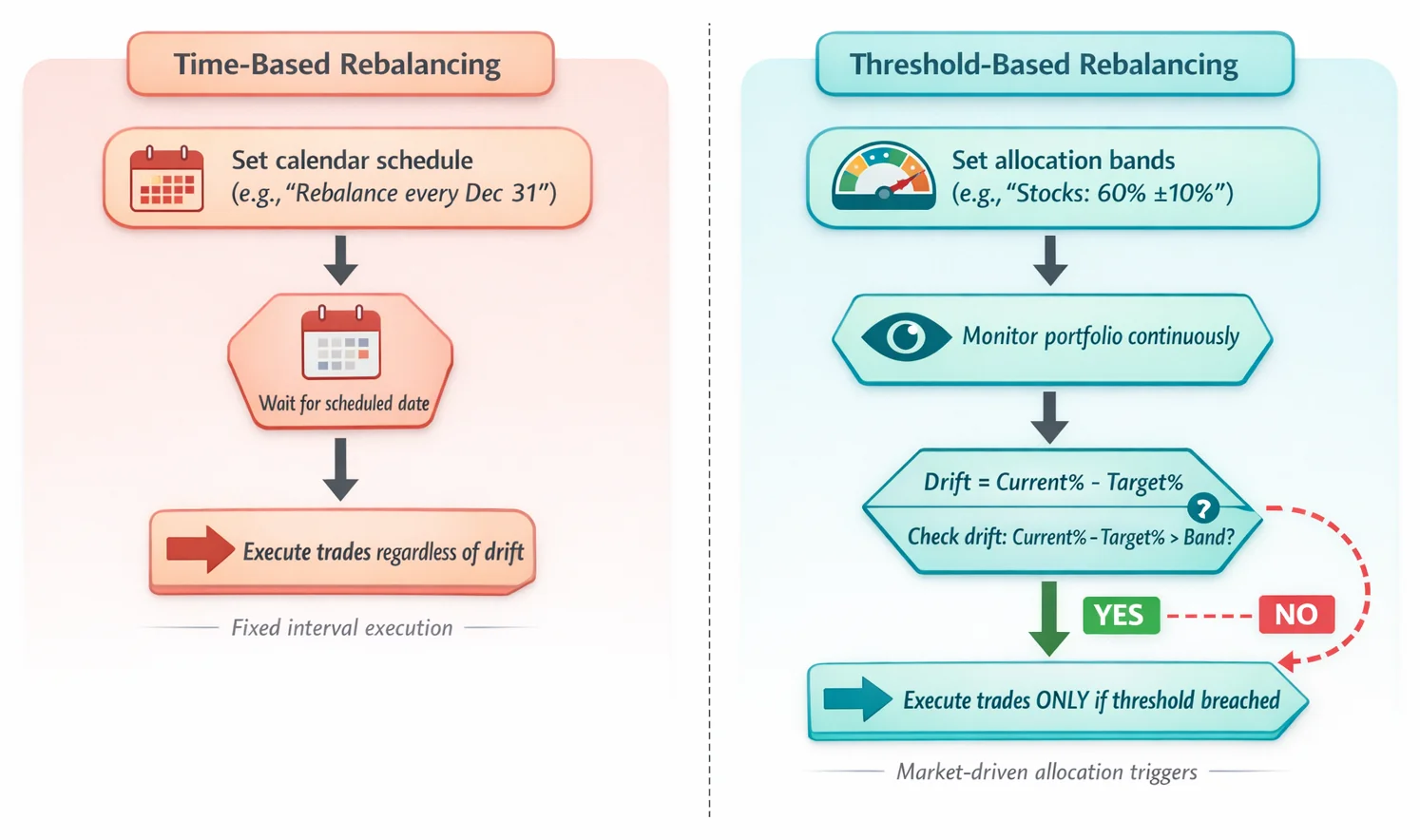

There are two main approaches:

- Time-based rebalancing: Adjusting at fixed intervals (e.g., annually or quarterly).

- Threshold-based rebalancing: Triggered only when an asset deviates from its target by a set band, like ±5% (a common threshold) or ±10% (a wider, less reactive band).

For ISA/SIPP investors, threshold-based rebalancing often outperforms rigid schedules. Wider bands (e.g., ±10%) reduce unnecessary trading, use tax-free efficiency, and minimise emotional tinkering, turning rebalancing into a powerful psychological tool rather than a technical chore. This aligns with modern portfolio theory principles, which you can explore in our guide to Markowitz Portfolio Optimisation.

Ultimately, rebalancing ensures your portfolio stays true to your strategy. Small, unaddressed drifts compound over time. Use our Compound Interest Calculator to see how even minor allocation shifts can impact long-term outcomes. By focusing on thresholds over timetables, you harness volatility to your advantage while letting ISAs and SIPPs handle the tax heavy lifting.

The Behavioural Secret: Why Frequency Matters Less Than Discipline

Forget everything you've heard about rigid rebalancing schedules. The truth is simpler and more powerful: portfolio rebalancing isn’t about timing the market or calendar alerts, it’s a behavioural tool to enforce discipline. While many obsess over "how often to rebalance a portfolio," research reveals that strict monthly or quarterly trades often backfire. Instead, trigger-based systems with wider allocation bands (like +/-10%) outperform by reducing emotional decisions and using the tax perks of ISAs and SIPPs.

Consider the myth that frequent rebalancing boosts returns. Vanguard's research, summarised by financial planner Michael Kitces, found that "rebalancing quarterly or monthly produced no improvement in long-term risk or returns; it simply drove up the turnover rate and the number of rebalancing events." Narrow thresholds force knee-jerk reactions to minor fluctuations, amplifying transaction costs and the temptation to "tweak" allocations based on fear or greed. Wider bands act as a psychological buffer, letting markets breathe while ensuring you only act when deviations meaningfully alter your risk profile.

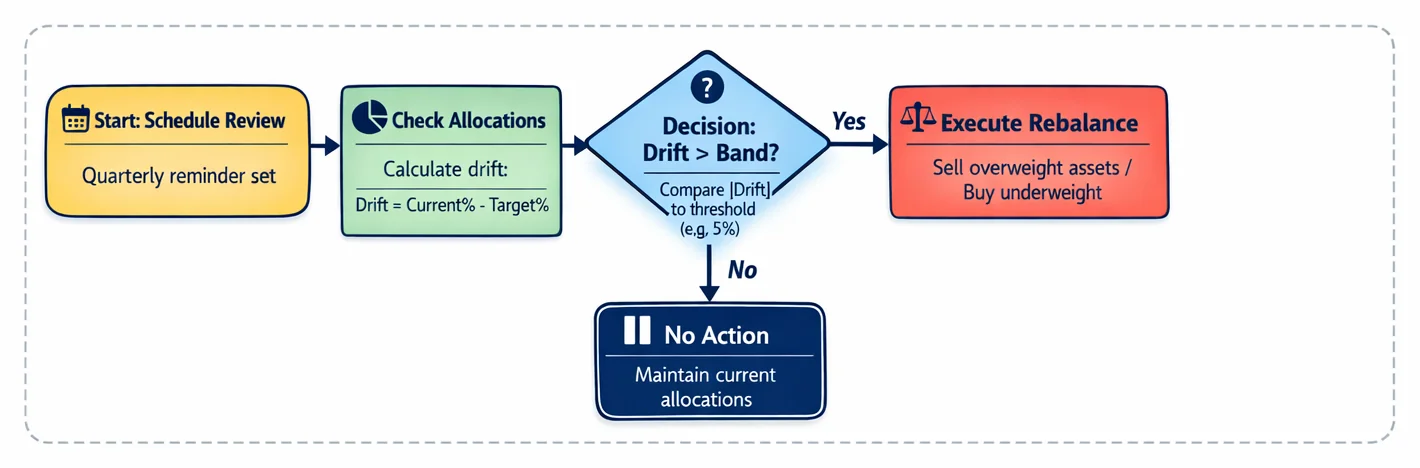

This is where hybrid rebalancing shines, a strategy combining scheduled reviews (e.g., quarterly check-ins) with threshold-based execution. The hybrid approach means checking your portfolio quarterly but only executing trades if the drift exceeds your set threshold (e.g., 5%). You maintain oversight without overtrading, locking in the core benefit: risk reduction. By preventing overexposure to surging assets (like stocks in a bull market), you systematically "buy low and sell high", a discipline proven to enhance long-term outcomes.

Critically, ISAs and SIPPs are ideal for this strategy. Unlike taxable accounts, these wrappers eliminate capital gains tax on rebalancing trades. You can adjust allocations friction-free, making threshold-based rebalancing cost-effective. Pair this with the well-documented finding that portfolios rebalanced annually have generated 0.35% to 0.50% higher returns than un-rebalanced ones by mitigating downturn risks, and the "less is more" advantage becomes clear.

Ultimately, rebalancing is less about frequency and more about fortitude. A wider band may only trigger trades during significant market swings, but each move capitalises on those moves. For perspective on how small return differences compound: £10,000 growing at 8% a year reaches roughly £21,589 in 10 years; a hypothetical 0.5% uplift from disciplined rebalancing would lift this to about £22,609 — a £1,020 difference. Tools like our Compound Interest Calculator let you model these increments yourself.

Embrace rebalancing as your behavioural anchor. Define your bands, use tax-free adjustments, and let markets come to you. For deeper insights on optimising risk-adjusted returns, explore our guide to the Sharpe Ratio or the principles of Markowitz Portfolio Optimisation. Ready to test your strategy? Our Portfolio Calculator lets you model band-based rebalancing scenarios tailored to UK investors.

ARIA PM automates threshold alerts and tax-efficient rebalancing across ISAs/SIPPs, freeing you to focus on strategy, not spreadsheets.

Step-by-Step: How to Rebalance Your UK Portfolio

Rebalancing isn’t about chasing market trends, it’s a behavioural discipline to buy low and sell high. Here’s how to execute it efficiently in your ISA or SIPP, using tax-sheltered accounts to avoid capital gains tax (a practice often called tax-sheltered prioritisation).

Set Your Target Allocations Start with a clear asset mix aligned to your goals and risk tolerance, e.g., 70% global stocks, 30% bonds. Use tools like our Portfolio Calculator to model scenarios. For deeper insights on balancing risk/return, explore Markowitz Portfolio Optimisation: Plain English.

Choose Your Rebalancing Strategy We recommend threshold-based rebalancing (e.g., act when an asset drifts ±10% from its target). This reduces emotional decisions and uses ISA/SIPP tax efficiency. Alternatives:

- Time-based: Review annually or semi-annually.

- Hybrid: Check quarterly but only act if drift exceeds 5%. Thresholds minimise unnecessary trading, critical during volatility.

- Calculate Drift Subtract your target allocation from the current percentage. For a £50,000 portfolio:

- Target: 60% stocks (£30,000), 40% bonds (£20,000).

- After a market rally: Stocks rise to £35,000 (70% of portfolio).

- Drift: 70%-60% = 10% (triggering rebalancing).

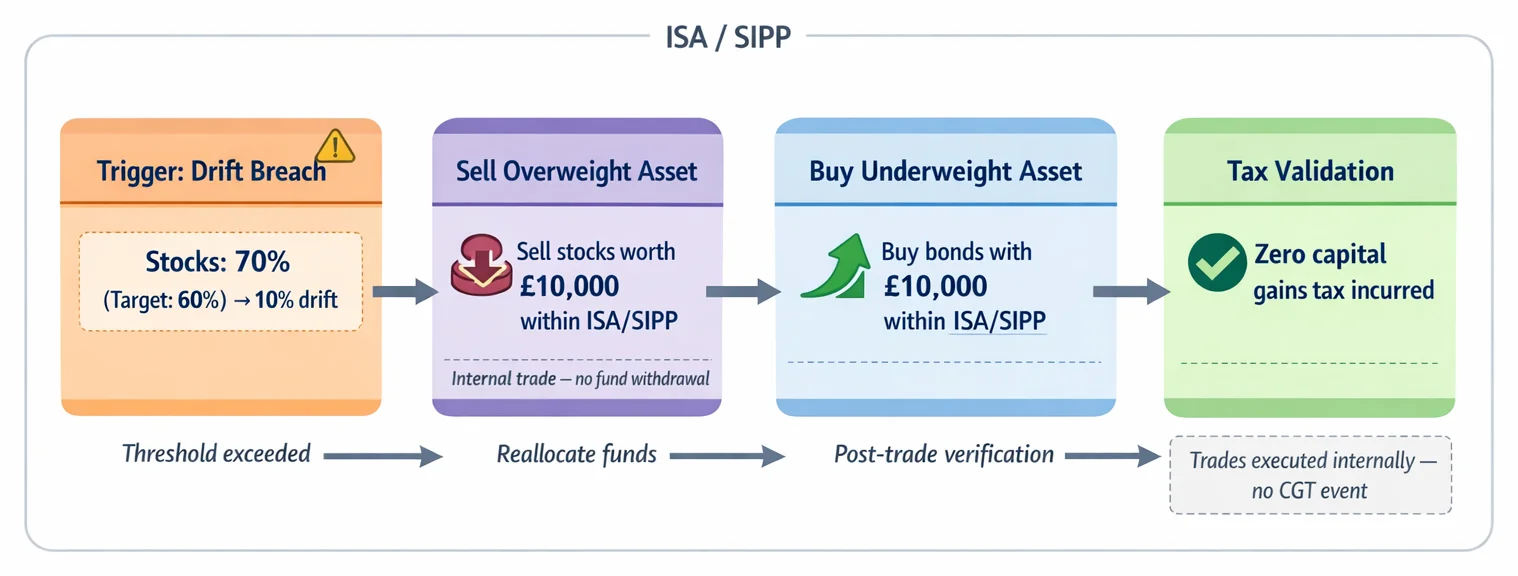

Execute Trades Tax-Efficiently Sell overweight assets (stocks in the example) and buy underweight ones (bonds), within your ISA or SIPP to avoid capital gains tax. UK-specific tip: From April 2027, the Cash ISA cap drops to £12,000 for under-65s. If you hold both Cash and Stocks & Shares ISAs, rebalancing might involve shifting funds between them to maximise your £20,000 allowance. For instance, redirect excess cash above £12,000 into underweight investments.

Document and Review Track dates, trades, and allocation changes. Research shows annually rebalanced portfolios historically delivered 0.35%-0.50% higher returns than un-rebalanced ones by systematically cutting risk exposure during downturns. Use our Compound Interest Calculator to project long-term impact.

Why This Works for UK Investors Threshold-based rebalancing in ISAs/SIPPs turns volatility into opportunity: you automatically buy lagging assets (low) and trim winners (high). Tools like our Sharpe Ratio Explained help quantify risk-adjusted gains. For complex portfolios, ARIA PM handles survivorship adjustment, cost modelling, and regime stress-testing automatically, so you focus on decisions, not data crunching.

Key Takeaway: Rebalancing is less about frequency, more about discipline. A ±10% band harnesses market swings without the stress of calendar rules, and the tax-free nature of ISAs/SIPPs makes it cost-effective.

Real-World Examples: How Platforms and Funds Handle Rebalancing

Putting rebalancing into practice varies across UK investment tools, each with distinct trade-offs between cost, control, and convenience. Crucially, the tax-free nature of ISAs and SIPPs eliminates capital gains tax on rebalancing trades, making band-based strategies (+/-10%) particularly efficient. Here’s how popular options compare:

1. Investment Platforms (Vanguard UK, Hargreaves Lansdown, AJ Bell) DIY platforms let you set custom allocation targets and visually track drift via dashboards. For example, AJ Bell highlights deviations like "UK Equities: 50% vs. Target 40%" if a 10% band is breached. However, most charge £5-£12 per trade, making frequent calendar-based rebalancing costly. A band approach minimises fees: rebalancing only when markets swing meaningfully (e.g., selling overweight winners to buy underweight assets). This aligns with our thesis, using bands as a behavioural circuit breaker against emotional decisions. Tools like our Portfolio Calculator help model these thresholds.

2. Robo-Advisors (Nutmeg, Wealthify) Robos automate rebalancing, typically at tighter 5% thresholds, for an ongoing platform and management fee (check each provider's current charges before committing). If your global equity allocation drifts above its target, they'll rebalance for you, removing behavioural friction entirely. However, those ongoing fees erode returns over time. For illustration, on a £50,000 portfolio a 0.6% annual fee would cost roughly £300 a year versus near-zero ongoing cost for DIY band rebalancing in an ISA/SIPP. Our Compound Interest Calculator shows how a small fee compounds: £10,000 growing at 7% a year reaches about £19,672 in 10 years, while the same pot at 6.4% (after a 0.6% fee) reaches roughly £18,622 — close to a £1,050 difference.

3. Target-Date Funds (Legal & General, Vanguard) These "set-and-forget" funds (e.g., "2050 Retirement Fund") handle rebalancing internally. Your £20,000 ISA contribution buys a single fund that automatically adjusts allocations to a glide path on the fund manager's schedule (some robo-advisor platforms, for example, top up holdings whenever uninvested cash exceeds a small threshold). While effortless, they offer zero customisation, problematic if your risk tolerance diverges from the fund’s glide path.

Regulatory Curveball: The 2027 Cash ISA Cap From April 2027, UK investors under 65 face a £12,000 annual limit on Cash ISA contributions. This restricts rebalancing flexibility if you routinely shift Stocks & Shares ISA holdings into cash. For example, selling £5,000 of equities and contributing it as new cash could breach the £12,000 cap if you’ve already contributed elsewhere. Over-65s retain the full £20,000 Cash ISA allowance, but younger investors must prioritise investment ISAs for larger rebalancing moves.

Key Takeaway Band-based rebalancing in ISAs/SIPPs combines tax efficiency with cost control, making it well suited to DIY investors. Robos offer automation but add fees, while target-date funds sacrifice flexibility for simplicity. As our guide on Markowitz Portfolio Optimisation explains, disciplined rebalancing maintains your intended risk-return profile. Use allocation bands to enforce "buy low, sell high" instincts, not market timing.

Internal links used: Portfolio Calculator, Compound Interest Calculator, Markowitz Portfolio Optimisation

5 Costly Rebalancing Mistakes Every Investor Makes

Rebalancing is meant to protect your portfolio, but common errors can turn it into a performance drag. For UK ISA and SIPP investors, avoiding these pitfalls is especially critical due to the tax-free advantages at stake. Here’s where investors go wrong:

Overtrading with Frequent Rebalancing: Reacting to every market wobble by rebalancing monthly or quarterly often backfires. Research shows this triggers excessive trading costs and forces you to sell winners too early. For example, a £100,000 portfolio rebalanced monthly could rack up several hundred pounds a year in trading fees alone, depending on your platform's per-trade charge. Solution: Use threshold-based rebalancing (e.g., only act when an asset deviates by 10% from target). Morgan Stanley's analysis of multiple rebalancing strategies found that pairing at-least-annual rebalancing with a 10% drift trigger improved annual returns by 0.24% and reduced annual volatility by 0.23% over a 10-year period compared with less disciplined approaches. UK robo-advisors like Nutmeg and Wealthify automate this using threshold triggers, making it effortless.

Ignoring Allocation Bands Altogether: Letting your 60% equity allocation balloon to 80% during a bull market feels great — until the crash hits. This turns your "balanced" portfolio into a high-risk gamble. Solution: Set clear rebalancing bands (+/-10% is a sensible starting point for most). If stocks surge to 70% in your 60% target ISA, that’s your cue to trim and buy underperforming assets. Remember: outside ISAs/SIPPs, frequent selling can trigger capital gains tax — making bands even more vital for taxable accounts.

Forgetting Cash in Your Allocation Math: Many investors exclude ISA cash buffers from their asset allocation. If you hold £20,000 in cash inside a £100,000 Stocks & Shares ISA "for emergencies," but only allocate the £80,000 invested, you’re distorting your risk profile. Solution: Treat cash as part of your fixed-income allocation. Use our Portfolio Calculator to include all holdings accurately. Remember: upcoming 2027 rules restricting transfers between ISA types make initial allocation even more critical.

Blindly Following the Calendar: Rebalancing every 1st January regardless of market conditions wastes effort and transaction fees if your portfolio hasn’t drifted meaningfully. Solution: Combine annual check-ins with threshold triggers. Only rebalance if assets breach your bands (e.g., 10% deviation). This "set and monitor" approach enforces discipline without unnecessary trades. For perspective, a 20% band still improves returns by 0.20% annually with lower volatility.

Overcomplicating Your Asset Classes: Splitting your portfolio into 7 niche ETFs with 2% rebalancing bands creates operational chaos. You’ll constantly trade tiny positions, eroding returns with fees. Solution: Consolidate into 3-4 broad categories (e.g., "Global Stocks," "UK Gilts," "Property"). Broader bands (5-10%) reduce noise. Tools like our Correlation Calculator help identify redundant holdings. As explained in our guide to Markowitz Portfolio Optimisation, simplicity often beats hyper-granularity.

The UK Advantage: Remember, ISAs and SIPPs eliminate the capital gains tax and dividend tax that punish frequent rebalancing in taxable accounts. This makes threshold-based rebalancing uniquely efficient. By setting intelligent bands and avoiding these traps, you transform rebalancing from a chore into a powerful behavioural tool — systematically buying low and selling high while your wrapper handles the tax heavy lifting. For deeper analysis on balancing risk and return, see our explainer on the Sharpe Ratio.

Your Rebalancing Action Plan: Next Steps for UK Investors

Now that you understand why rebalancing matters, and why it’s more about psychology than precision, let’s turn theory into action. Follow these practical steps to build discipline and use your ISA/SIPP’s tax efficiency:

Log in and note your current allocations Open your ISA or SIPP dashboard immediately. Record each asset class’s current percentage (e.g., "UK equities: 65%, bonds: 30%, cash: 5%"). This baseline reveals your actual risk exposure. With markets volatile in 2025, deviations may be wider than you think.

Set or confirm your target allocation Align targets with your risk tolerance. If you’re unsure, use our Portfolio Calculator to model scenarios. Remember: a 60% equity/40% bond split is common, but not universal. As the Wellington US Institutional study confirmed, any disciplined rebalancing beats neglecting it entirely.

Choose your strategy: Thresholds beat calendars Opt for threshold-based rebalancing (e.g., act only when an asset drifts ±10% from target). This mirrors institutional tactics like Morgan Stanley’s 10%-20% bands, cutting unnecessary trades. For hands-off investors, a hybrid approach works: check quarterly but only adjust if thresholds are breached.

Schedule reminders, not automatic trades Set quarterly calendar alerts to review allocations, but rebalance only if needed. Annual deep dives are fine for stable markets. Crucially, 2026’s projected volatility makes threshold checks urgent now: delaying could amplify drift.

Use free tools to track drift Most UK platforms (e.g., Vanguard, Hargreaves Lansdown) show allocation dashboards. For deeper analysis, tools like Morningstar’s portfolio tracker (accessible via our Free Tools hub) automate drift alerts.

Post-rebalancing review: Ask one question After adjusting, reflect: "Did I sell high and buy low?" For example: trimming equities after a 15% rally to buy undervalued bonds. This enforces the behavioural win.

Why This Works for ISA/SIPP Investors

Tax-free wrappers eliminate capital gains taxes on rebalancing, making threshold strategies more efficient than in taxable accounts. Pair this with volatility reduction: institutional data shows band-based rebalancing can lower annual volatility by 0.23%-0.24%, smoothing returns without sacrificing growth.

While one study found quarterly rebalancing beat annual by 1.5% over a decade, overtrading erodes gains through fees and behavioural missteps. Thresholds prevent this. For complex portfolios, tools like ARIA PM handle survivorship adjustment and stress-testing automatically, letting you focus on decisions, not data crunching.

Reinforce the discipline: Your portfolio isn’t a machine needing quarterly oil changes. It’s a behavioural pact to buy low and sell high. As 2026’s uncertainty looms, your greatest edge is patience, not a calendar.

Key takeaway: Log in today. Set your ±10% bands. Let markets move, you’ll act only when it counts.

Deepen your strategy: Understand the theory behind allocations with our plain-English guide to Markowitz Portfolio Optimisation or gauge risk efficiency via the Sharpe Ratio.

Key Takeaways

- For your ISA or SIPP, use threshold-based rebalancing (e.g., triggering trades only when an asset class deviates by ±10% from its target) primarily as a behavioural tool to enforce disciplined buying low and selling high.

- Use the tax-free nature of your ISA and SIPP to rebalance without capital gains tax penalties, making threshold-based adjustments particularly cost-effective.

- Focus rebalancing on controlling your portfolio's risk exposure, not chasing higher returns, by systematically returning to your original asset allocation targets after market moves.

- Wider rebalancing bands (±10%) often prove more effective than rigid calendar schedules, reducing unnecessary trading and emotional decision-making during normal volatility.

- Implement rebalancing mechanically to counteract the instinct to chase rising markets or panic-sell during downturns, locking in gains from winners and buying assets when they are relatively cheaper.

| Feature | Calendar-Based Rebalancing | Band-Based Rebalancing (+/-10%) | Why Band-Based Wins for ISA/SIPP |

|---|---|---|---|

| Trigger Mechanism | Fixed time intervals (e.g., quarterly/annual) | Deviation from target allocation | Acts only during meaningful market moves |

| Behavioural Impact | May force unnecessary trades in calm markets | Enforces "buy low/sell high" during volatility | Reduces emotional decisions by trading less frequently |

| Tax Efficiency | Potential CGT in taxable accounts | Zero CGT impact in ISAs/SIPPs | Uses tax-free wrappers for frictionless adjustments |

| Performance Impact | Higher transaction costs over time | Lower costs, avoids overtrading | Preserves capital by minimising unnecessary trades |

| Best For | Passive investors needing structure | Disciplined investors embracing volatility | UK investors using tax-sheltered accounts |

Platform Rebalancing Features: Control vs. Convenience

| Platform Type | Rebalancing Method | Investor Control | Cost Implications | Best For |

|---|---|---|---|---|

| DIY Platforms | Manual trades | Full control | Free or low-cost trades | Hands-on investors using band-based strategies |

| Robo-Advisors | Automatic, rules-based | Limited control | Management fees | Passive investors preferring automation |

| Fund Managers | Built-in rebalancing (e.g., multi-asset funds) | No control | Ongoing charges | Investors prioritising simplicity |

| Key ISA/SIPP Benefit | All methods avoid capital gains tax during rebalancing | Maximises tax-free compounding |

Sources

- FCA: InvestSmart, FCA guidance on core investment principles, including diversification and ongoing portfolio management for UK investors.

- MoneyHelper: Investing, UK government-backed advice hub on investing and managing portfolios like ISAs/SIPPs.

- Vanguard UK: Rebalancing your portfolio, Evidence-based strategies for rebalancing frequency and methods from a major UK platform provider.

- Hargreaves Lansdown: Reviewing your investment portfolio, Practical steps for reviewing and rebalancing within tax-efficient wrappers like ISAs/SIPPs.

- SEC: Rebalancing Your Portfolio, Foundational principles of rebalancing from the US regulator, applicable to UK investors.

- Charles Stanley: How to review your investment portfolio, Tactical approaches to reviewing and rebalancing, including triggers and UK tax considerations.