You’ve carefully chosen your investments, but are you unknowingly losing thousands by holding them in the wrong ISA or SIPP wrapper? Many UK investors focus solely on their overall risk level when building a portfolio, overlooking a critical factor: tax treatment. This mistake can erode your long-term returns significantly. This article explains how an Asset Allocation Calculator becomes your essential tool, not just for setting risk-based targets, but for strategically placing assets across your ISA and SIPP to maximise what you actually keep after tax. You’ll learn why the tax-free growth of an ISA and the upfront tax relief but later taxation of a SIPP fundamentally change where specific assets should sit. Discover how optimising asset location, guided by a calculator, is as vital as choosing the assets themselves for building true wealth.

What is an Asset Allocation Calculator? Your Tax Efficiency Secret Weapon

Most investors spend hours agonising over their risk tolerance — debating stock vs. bond percentages, fretting over market dips. Yet, they often overlook a far more powerful wealth-builder: tax efficiency. This is where an asset allocation calculator transforms from a basic risk tool into your secret weapon for maximising long-term returns in UK accounts like ISAs and SIPPs.

At its simplest, an asset allocation calculator is a digital tool that suggests how to split your portfolio across different assets — like shares, bonds, or alternatives — based on your age, goals, and comfort with volatility. But here’s the critical shift: for ISA and SIPP investors, its primary role isn’t just setting risk-based targets. It’s a tax-optimisation engine designed to dynamically place specific assets across these wrappers to maximise your after-tax terminal wealth.

Why is this perspective non-obvious but crucial? Because ISAs and SIPPs have radically different tax treatments. ISAs offer completely tax-free growth and withdrawals — no capital gains tax, no dividend tax, no income tax. SIPPs provide tax-deferred growth — you get upfront tax relief on contributions, but pay income tax on withdrawals in retirement. This means where you hold an asset (ISA vs. SIPP) can dramatically impact your final savings, often more than the asset’s raw return. Holding high-growth equities in your ISA shields all gains from tax forever, while placing income-heavy assets strategically in your SIPP can use tax relief now and potentially lower rates in retirement.

Consider how investment strategies evolve. The traditional 60/40 portfolio (60% shares, 40% bonds) is increasingly supplemented with private and alternative assets, especially in larger portfolios. But even a modern mix fails if you don’t consider location. A high-yield bond fund held in the wrong wrapper can lose a meaningful share of its return to tax drag over decades, while the same fund optimally placed compounds unimpeded. This is why calculators must model not just what you own, but where it lives.

The compounding effect magnifies this. Imagine two investors with identical £50,000 portfolios growing at 6% annually for 30 years. One uses a basic risk-only calculator, the other optimises asset location for tax efficiency. Even a 0.5% annual tax drag difference — from inefficient placement — could cost the first investor over £30,000 in terminal wealth. Tools like our Compound Interest Calculator vividly show how small savings snowball.

This is the "aha" moment: Your ISA and SIPP aren’t interchangeable buckets. They’re complementary tools requiring strategic asset placement. A sophisticated calculator factors in UK tax rules, simulates growth across decades, and adjusts for your personal tax bracket — turning allocation from a static risk exercise into dynamic tax engineering. For deeper theory, explore our guide to Markowitz Portfolio Optimisation: Plain English, which underpins these calculations. Platforms like ARIA PM automate this complexity, integrating tax dynamics so you can focus on outcomes, not spreadsheets. Combine this with understanding risk metrics like the Sharpe Ratio, and you’re not just building a portfolio — you’re building tax-optimised wealth.

Why ISA and SIPP Tax Rules Change Everything for Your Allocation

Forget everything you thought you knew about asset allocation. While risk tolerance matters, the real significant improvement for UK investors is how ISA and SIPP tax rules interact with your investments. Why? Because these wrappers treat growth and income radically differently — and misplacing assets could cost you thousands in lifetime wealth.

Start with the basics:

- ISAs offer tax-free growth and withdrawals. You pay no capital gains tax, dividend tax, or income tax on anything held inside them.

- SIPPs provide tax-deferred growth — meaning no immediate taxes on dividends or capital gains — but withdrawals are taxed as income in retirement (typically at 20% or 40%).

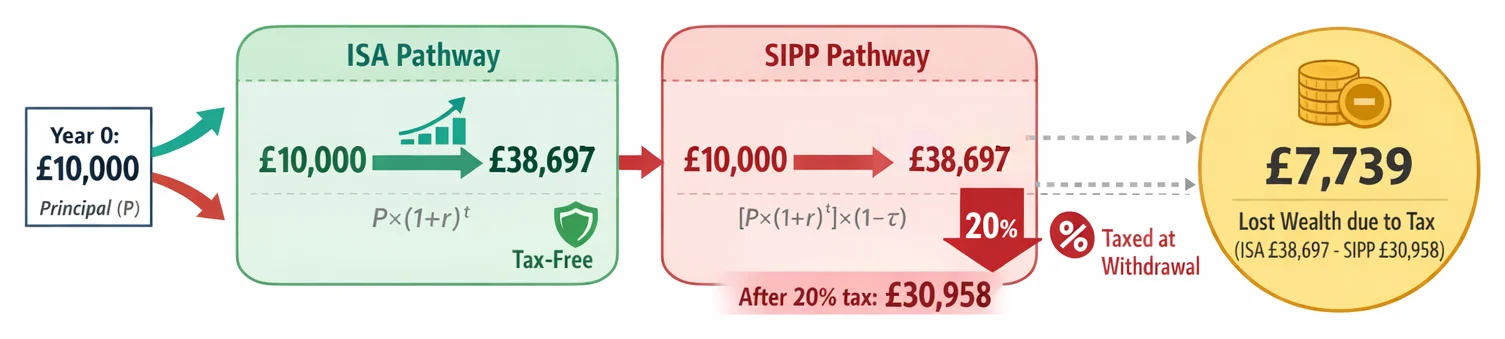

This split creates a tax-efficiency puzzle. High-growth assets like equities thrive in ISAs. Why? Compounding works unimpeded. Imagine £10,000 in global stocks growing at 8% annually. After 20 years in an ISA, it becomes £46,610 — all yours tax-free. In a SIPP, that same pot could shrink by £9,322 (assuming 20% tax on withdrawal) or £18,644 (at 40%).

Conversely, income-heavy assets like bonds often fare better in SIPPs. Bond interest is taxed annually in taxable accounts (or ISAs, though tax-free). But in a SIPP, that income compounds tax-deferred until retirement, when you might be in a lower tax bracket. For example: £10,000 in bonds yielding 4% annually would generate £400 yearly income. Outside an ISA, a higher-rate taxpayer loses £160 annually to tax — draining £3,200+ over 20 years before growth. In a SIPP, that leakage stops.

Now layer in real-world complexity. High-net-worth (HNW) portfolios aren’t just stocks and bonds. They often hold a substantial share in private and alternative assets like private equity or hedge funds. These alternatives often generate "unfriendly" income (e.g., interest taxed at income rates) or irregular gains. Placing them in the wrong wrapper amplifies tax drag. A private equity fund returning 12% annually in an ISA? All gains are shielded. In a SIPP? Gains compound tax-deferred, but a 40% withdrawal tax bite could erase years of growth.

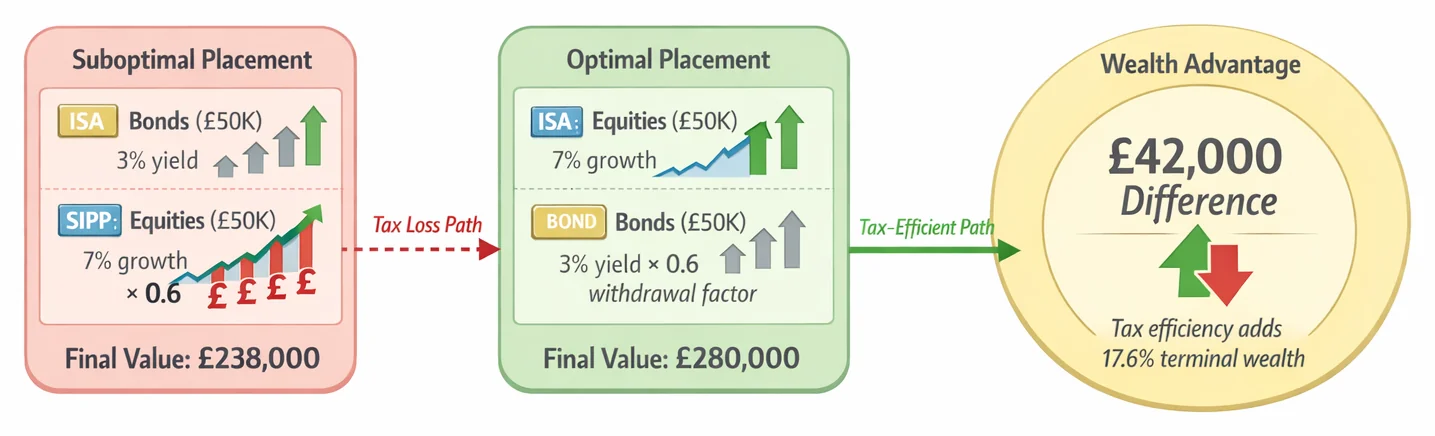

The ‘aha’ moment: Asset location isn’t secondary — it’s foundational. Poor placement doesn’t just dent returns slightly; it sabotages compounding. Consider two investors each hold £50,000 in equities (7% growth) and £50,000 in bonds (3% yield).

- Investor A holds bonds in ISA (tax-free income), equities in SIPP (40% tax on withdrawal).

- Investor B holds equities in ISA (tax-free growth), bonds in SIPP (40% tax on income at withdrawal).

After 25 years, Investor B’s portfolio is worth £42,000 more after tax. Why? The high-growth engine (equities) ran tax-free, while bonds’ lower-growth income faced deferred taxation.

This is where an asset allocation calculator transforms from a risk tool to a tax-engineering engine. It doesn’t just suggest "60% stocks, 40% bonds." It dynamically models:

- Which assets belong in ISA vs. SIPP based on growth potential, yield, and your tax bracket.

- How shifting tax rules (e.g., dividend allowances) impact long-term outcomes.

- The role of alternatives — increasingly common in HNW portfolios — in cross-wrapper optimisation.

Tools like our Compound Interest Calculator reveal the staggering cost of tax drag, while concepts from Markowitz Portfolio Optimisation help balance risk within this tax-aware framework.

Bottom line: Optimising allocation without considering ISA/SIPP tax rules is like building a sports car with the engine in the boot. The calculator’s job? Ensure every asset sits where it revs hardest — tax-free.

Explore more tactical tools in our Free Tools hub, or deepen your strategy with the Sharpe Ratio Explained.

How to Use an Asset Allocation Calculator: Step-by-Step UK Guide

An asset allocation calculator transforms tax efficiency from theory into practice for your ISA and SIPP. Unlike basic tools focusing solely on risk, it dynamically places assets across your wrappers to maximise after-tax wealth. Here’s how to use it effectively:

Step 1: Input Personal Factors

Start with your age, investment goals (e.g., retirement age, target income), and risk tolerance. Many UK investors use the ‘110-minus-age’ rule as a starting point for equity exposure (e.g., a 40-year-old might allocate 70% to equities). This sets your overall risk profile. Crucially, your time horizon directly impacts how the calculator prioritises tax-deferred growth in your SIPP versus tax-free withdrawals in your ISA.

Step 2: Define Wrapper Sizes

Specify current balances in your ISA and SIPP. The relative size of these wrappers drives tax optimisation. For example, a £50K ISA and £70K SIPP creates different placement opportunities than a £100K ISA and £20K SIPP. The calculator uses this to prioritise which assets go where — using the ISA’s tax-free growth for high-return assets and the SIPP’s upfront tax relief for income-generating holdings.

Step 3: Select Assets

Choose assets aligning with your strategy. Beyond standard equities and bonds, consider:

- Alternatives: Including cryptocurrency, which has become a more common holding among high-net-worth and younger investors.

- Fixed income: Re-evaluate bonds strategically — rising yields may enhance diversification against equities. High-net-worth investors typically hold a large share of their investable portfolio in public equities, with alternatives making up a growing slice at the very top of the wealth scale.

Step 4: Interpret & Implement the Output

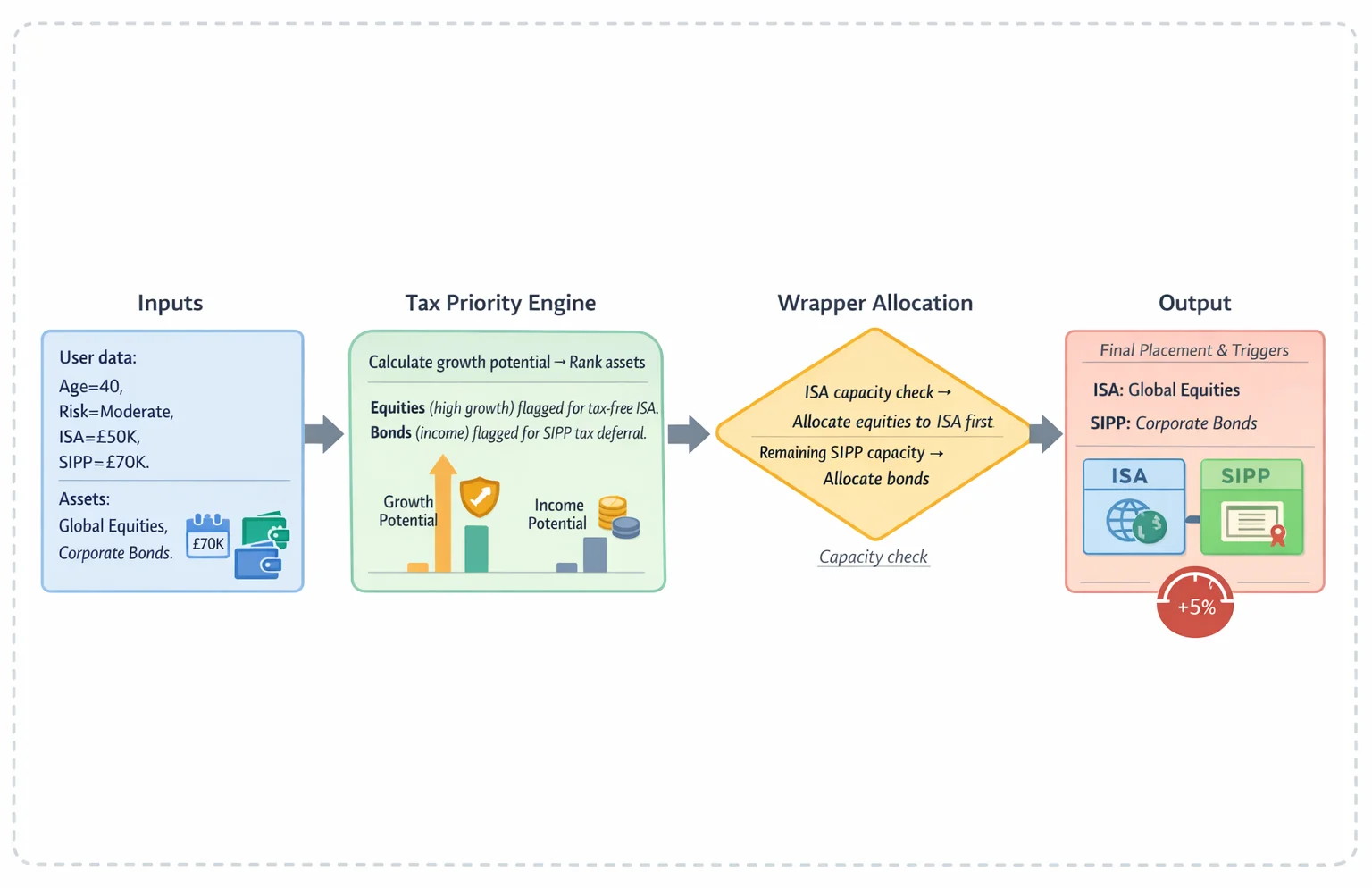

The calculator generates a dynamic placement strategy, not just static percentages. For instance:

A 40-year-old with £50K ISA and £70K SIPP might place global equities in the ISA (exploiting tax-free growth) and corporate bonds in the SIPP (using tax deferral on income).

Key outputs include:

- Asset location map: Shows precisely which assets belong in each wrapper.

- Tax-adjusted growth projection: Illustrates how placement boosts terminal wealth.

- Rebalancing triggers: Flags when to adjust — e.g., age milestones (like approaching 55), or market shifts altering your allocation by >5%.

Maintaining Your Allocation

Rebalance annually or when:

- Your age-based equity allocation changes (e.g., shifting from 70% to 65% equities at age 45).

- Market movements disproportionately grow one asset class.

- Contributions alter your ISA/SIPP balance ratio.

Tools like our Correlation Calculator help monitor asset relationships, while understanding the Sharpe Ratio clarifies risk-adjusted returns. For deeper theory, explore Markowitz Portfolio Optimisation.

ARIA PM handles survivorship adjustment, cost modelling, and regime stress-testing automatically — so you focus on implementing your personalised, tax-engineered strategy. Test your target mix using our Free Tools, and project long-term growth with the Compound Interest Calculator.

Next, we explore common pitfalls in ISA/SIPP allocation — and how to avoid them.

Real-World Examples: Optimising Popular Assets Across ISA and SIPP

Forget the old mantra that asset allocation is purely about balancing risk. In the UK, your ISA and SIPP wrappers transform it into a tax-engineering challenge. The goal? Maximise after-tax terminal wealth by dynamically placing assets where their growth or income faces the lightest tax burden. Let’s break this with concrete examples:

Global Equities (Prioritise ISA for Growth) Equities thrive on compounding, making the ISA’s tax-free growth ideal. Consider £50,000 in a global index fund. In an ISA, 7% annual growth over 20 years becomes £193,482 tax-free. In a SIPP, even with 20% upfront tax relief, a basic-rate taxpayer withdrawing the same amount pays £38,696 in income tax — leaving £154,786. That’s a £38,696 difference. For non-US equities (like undervalued European or Japanese stocks), this advantage amplifies — their cyclical growth potential compounds tax-free.

Government Bonds (Consider SIPP for Income) Bonds generate taxable interest. A SIPP defers this tax until withdrawal, which may align with lower retirement rates. Imagine £30,000 in UK gilts yielding 4% annually. In a taxable account, a higher-rate taxpayer pays 40% tax on that interest (£480 tax on £1,200 interest, beyond the personal savings allowance). In a SIPP, the full £1,200 compounds annually. If withdrawn later at a basic rate, you keep more of the compounded sum — often beating a taxable account.

REITs (ISA to Avoid Income Tax) REITs must distribute 90% of income as dividends, taxable at your marginal rate outside tax wrappers. Holding them in an ISA shields this income. A £20,000 REIT yielding 5% pays £1,000 annually. In an ISA, you keep it all; in a taxable account, a higher-rate taxpayer surrenders £400 yearly to HMRC. Over 10 years, that’s £4,000 lost — plus forfeited compounding.

Alternatives & Crypto (Mind ISA Eligibility) High-volatility assets like crypto benefit enormously from tax-free growth, but most cannot be held directly inside an ISA or SIPP. Check wrapper eligibility before assuming a speculative asset can sit tax-free — you may need to use an exchange-traded product or fund that does qualify.

The Pitfall of Static Allocation

A rigid "60% equities, 10% bonds, 30% alternatives" split ignores tax dynamics. Take two investors with identical £100,000 portfolios:

- Investor A uses static allocation: REITs and bonds in SIPP, equities in ISA.

- Investor B optimises tax placement: equities and REITs in ISA, bonds in SIPP. After 20 years, Investor B’s after-tax wealth could be materially higher due to sheltered REIT income and equity growth.

Why Location Trumps Allocation

Tax efficiency interacts with broader strategy. During inflationary phases, dynamic allocation might shift you toward commodities or inflation-linked bonds. But without optimising wrapper placement — e.g., holding inflation bonds in a SIPP to defer tax on income — much of the gain leaks away. Similarly, geographical diversification into European or EM equities only delivers full potential if housed in ISAs.

Platforms like Vanguard or Hargreaves Lansdown offer tools to model these placements, but our asset allocation calculator integrates tax rules, compounding, and regime shifts. Pair it with our compound interest calculator to quantify tax savings, or explore the theory behind optimising returns in our guide to Markowitz Portfolio Optimisation. Remember: your risk tolerance sets the what, but tax alignment decides the where — and that’s the difference between theoretical gains and real wealth.

Top 5 ISA/SIPP Allocation Mistakes (and How to Fix Them)

Building a reliable portfolio across your ISA and SIPP isn't just about picking assets — it's a strategic tax-optimisation game. Many investors focus solely on risk tolerance while overlooking how asset placement impacts long-term wealth. Here are five critical missteps and how to correct them:

Mistake: Ignoring Tax Wrapper Properties Treating ISA and SIPP as interchangeable buckets wastes their unique advantages. ISAs offer tax-free growth and withdrawals, making them ideal for high-growth assets like equities. SIPPs provide tax-deferred compounding but incur income tax on withdrawals, favouring assets generating taxable income (like bonds). Fix: Map assets strategically. Prioritise equities in your ISA to shield maximum growth from tax. Hold income-generating assets like bonds in your SIPP to defer tax on dividends/interest. Use an asset allocation calculator to model placement scenarios.

Mistake: Isolating Wrappers Instead of Viewing the Whole Portfolio Managing ISA and SIPP as separate portfolios leads to overlapping holdings, inefficient diversification, and missed tax synergies. Fix: Consolidate your view. Analyse all holdings across wrappers as one unified portfolio. Tools like our Correlation Calculator help assess diversification holistically, while Markowitz Portfolio Optimisation principles ensure efficient risk/return balance across accounts.

Mistake: Static 'Set-and-Forget' Allocation Relying on rigid rules like the 110-minus-age heuristic (equity % = 110 minus your age) ignores life changes, tax shifts, and market regimes. Allocations to bonds, cash, and alternatives shift as markets evolve, and outdated assumptions about bond-equity correlations can prove risky in a higher-inflation environment. Fix: Review allocations annually. Adjust for age, income shifts, and regime changes. ARIA PM handles survivorship adjustment, cost modelling, and regime stress-testing automatically — so you can focus on interpreting results rather than building the simulation.

Mistake: Chasing Trends Without Tax Planning Adding speculative assets (e.g., crypto) to wrappers without verifying rules invites penalties or simply finding the asset is ineligible. Many speculative assets cannot be held directly inside an ISA or SIPP. Fix: Always check wrapper eligibility before buying. If holding cash temporarily, use a cash ISA where appropriate. For eligible volatile assets, prioritise ISAs to lock in tax-free gains.

Mistake: Underestimating Fees in Alternatives Failing to factor costs of REITs, funds, or managed services into returns erodes compounding. For instance, £10,000 growing at 8% annually for 20 years becomes £46,610. At 7.5% (just 0.5% lower), it drops to £42,479 — a £4,131 difference. Fix: Scrutinise all fees. Use our Compound Interest Calculator to model fee impacts. Prioritise low-cost trackers unless active funds consistently justify fees via Sharpe Ratio outperformance after costs.

By treating allocation as a dynamic tax-engineering exercise — not just risk calibration — you transform your ISA and SIPP into a unified wealth accelerator. Regularly revisit your strategy with tools like our Investment Calculator to stay aligned with life stages and tax landscapes.

Your Next Steps: Building a Tax-Smart Portfolio Today

Now that you understand why tax efficiency drives optimal ISA and SIPP allocation — not just risk tolerance — it’s time to act. Follow this four-step action plan to transform your portfolio from tax-inefficient to strategically engineered.

1. Audit your current holdings immediately Gather your latest ISA and SIPP statements. Scrutinise where each asset sits:

- Are high-growth equities (like global stocks) in your ISA, maximising tax-free compounding?

- Are bonds or cash reserves tucked in your SIPP, using tax-deferred growth?

- Crucially, review cash in Stocks & Shares ISAs: holding large cash balances in an investment wrapper forgoes growth potential. If you hold significant cash there, consider whether it belongs in a cash account or invested in bonds or equities instead.

2. Use free calculators to model scenarios Tools like Morningstar’s asset allocation calculator let you simulate outcomes based on:

- Your age and time horizon: Start with the "110-minus-age" rule. A 40-year-old with moderate risk tolerance might begin at 70% equities, adjusting to 60% (conservative) or 80% (aggressive).

- Tax wrappers: Input your ISA/SIPP split to see how shifting assets impacts after-tax wealth. For example, holding FTSE 100 equities in an ISA can save a substantial sum in dividend and capital gains tax over 20 years versus a taxable account.

- Diversification: Model adding European or emerging markets (EM) equities — historically less correlated with UK assets — using our Correlation Calculator to test their impact.

3. Start simple, then refine Prioritise progress over perfection:

- Basic rule: Equities in ISA (tax-free growth), bonds in SIPP (tax-deferred income).

- Adjust for age: If you’re 50, "110-minus-age" suggests 60% equities. Pair this with a 60/40 ISA/SIPP split if retirement is near.

- Optimise incrementally: Use our Investment Calculator to compare outcomes. £10,000 growing at 7% annually in an ISA becomes £19,672 in 10 years; at 6.5% in a taxable account, it’s £18,771 — a £901 gap from taxes alone.

4. Schedule rebalancing & review Tax laws and markets shift. Twice yearly:

- Rebalance holdings to your target mix (e.g., sell overperforming ISA assets to buy underweight SIPP bonds) — the portfolio rebalancing calculator turns that target mix into the exact buy and sell amounts.

- Review asset location: avoid holding large cash balances in a Stocks & Shares ISA. Shift high-yield bonds to SIPPs if income tax efficiency improves.

- Stress-test using our Sharpe Ratio Explained guide to ensure risk-adjusted returns align with new allocations.

Why this compounds wealth Tax-aware allocation isn’t a one-time fix — it’s a compounding advantage. Every pound saved from unnecessary tax in your ISA grows exponentially. For instance, shifting £20,000 from a taxable account to an ISA can add a meaningful sum over 20 years at 7% growth, by sheltering dividends and gains that would otherwise be taxed.

Diversify strategically: European and EM equities offer growth potential, but always prioritise tax placement first. For advanced optimisation, explore Markowitz Portfolio Optimisation principles — or use tools like ARIA PM, which handles survivorship bias, cost modelling, and regime stress-testing automatically, letting you focus on strategy.

Your move this week: Calculate your ISA/SIPP ratio using our Free Tools, then relocate one tax-inefficient asset. Small steps today forge monumental gains tomorrow.

Key Takeaways

- Prioritise tax efficiency over risk tolerance when using an asset allocation calculator for your ISA and SIPP, as its core function is maximising after-tax wealth through strategic asset placement.

- Place high-growth assets like equities primarily within your ISA to shield all future capital gains and dividends from tax permanently.

- Allocate tax-inefficient assets generating significant income (like bonds or REITs) strategically within your SIPP to use upfront tax relief and potentially lower income tax rates in retirement.

- Understand that your optimal ISA/SIPP asset mix must dynamically adapt as tax rules, your portfolio size, or retirement income needs change over time.

- Recognise that correctly locating assets between your ISA (tax-free) and SIPP (tax-deferred) using the calculator can significantly outperform a static allocation based solely on risk.

| Feature | Traditional Approach | Tax-Optimised Approach |

|---|---|---|

| Primary Goal | Match risk tolerance | Maximise after-tax terminal wealth |

| Asset Placement | Ignores tax wrappers | Strategically locates assets across ISA/SIPP |

| Key Driver | Risk capacity & time horizon | Tax rules (ISA tax-free vs. SIPP tax-deferral) |

| Calculator Role | Sets static stock/bond ratios | Dynamically models tax impact across wrappers |

| Wealth Impact | Suboptimal due to tax drag | Materially higher terminal wealth (compounding effect) |

ISA Treatment vs. SIPP Treatment: Asset Placement Guide

| Asset Type | ISA Advantage | SIPP Advantage | Optimal Placement Strategy |

|---|---|---|---|

| Growth Stocks | Tax-free capital gains | Tax-deferred growth | Prioritise ISA to shield high-growth assets |

| Dividend Shares | Tax-free dividend income | Tax-deferred dividends | ISA first (avoid dividend tax entirely) |

| Government Bonds | Tax-free interest | Upfront tax relief | SIPP preferred (lower growth = less future tax) |

| REITs/Property | Tax-free rental income | Tax-deferred income | ISA first (high yield benefits more from tax-free) |

| Corporate Bonds | Tax-free interest | Tax relief on contributions | SIPP preferred (offset taxable interest elsewhere) |

Sources

- FCA: Investment Diversification — FCA guidance on spreading investments across assets to manage risk in portfolios.

- SEC: Asset Allocation — SEC’s investor education on balancing risk and return through diversified investments.

- MoneyHelper: Choosing investments — UK government-backed advice on building portfolios for ISAs and pensions.

- Vanguard: Investor Questionnaire — Risk-assessment tool suggesting personalised allocations for ISA/SIPP investments.

- Hargreaves Lansdown: Calculators — HL's hub of investment calculators and planning tools for ISA/SIPP investors.

- Investopedia: Asset Allocation — Comprehensive guide to allocation strategies and model portfolios.