Imagine a UK investor carefully building a "mathematically optimal" portfolio using standard software, only to face a significant, unexpected tax bill that erases much of their calculated gains. This frustrating scenario is common when tools designed for generic markets overlook the profound impact of UK tax rules. For UK investors, the difference between pre-tax theory and post-tax reality can mean thousands of pounds lost annually or crucial retirement goals missed. This article answers a critical question: What specific features make Portfolio Optimisation Software for UK Investors genuinely effective for maximising your real-world wealth? We'll explain why the most powerful tool isn't necessarily the one with the most complex algorithms, but the one that deeply integrates UK-specific elements like ISAs, SIPPs, dividend taxation, and Capital Gains Tax allowances directly into its core calculations. This fundamental shift prioritises your actual, spendable returns over misleading pre-tax metrics.

What Portfolio Optimisation Software Is and Why UK Investors Need It

Building an investment portfolio can feel overwhelming. With thousands of assets, shifting markets, and complex UK tax implications, how do you confidently choose the right mix? This is where portfolio optimisation software steps in. These digital tools use mathematical algorithms — often based on Nobel Prize-winning concepts like the efficient frontier — to calculate the ideal asset allocation for your specific risk tolerance and financial goals. At its core, they answer a critical question: "What combination of investments gives me the highest expected return for the level of risk I’m willing to accept?"

The demand for these tools has grown steadily as investors seek data-driven decisions over gut feeling. Modern solutions often incorporate AI and machine learning for predictive analytics and automated rebalancing, while cloud-based platforms enable flexible access from any device.

But here’s the critical gap for UK investors: most generic optimisation tools ignore the tax rules that make or break your actual returns. They prioritise pre-tax volatility metrics like the Sharpe ratio, but this fundamentally misrepresents "risk" and "return" in a UK context. Why? Because UK tax structures drastically alter your net outcomes:

- Dividends outside an ISA face a £500 annual allowance (2024/25), then tax at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate). Inside an ISA, they’re entirely tax-free.

- Capital gains on shares incur an 18% or 24% tax rate after a £3,000 annual exempt amount. Gains within an ISA are completely shielded from Capital Gains Tax.

- Even buying UK shares triggers a 0.5% Stamp Duty Reserve Tax (SDRT) — a £10,000 trade costs £50 upfront.

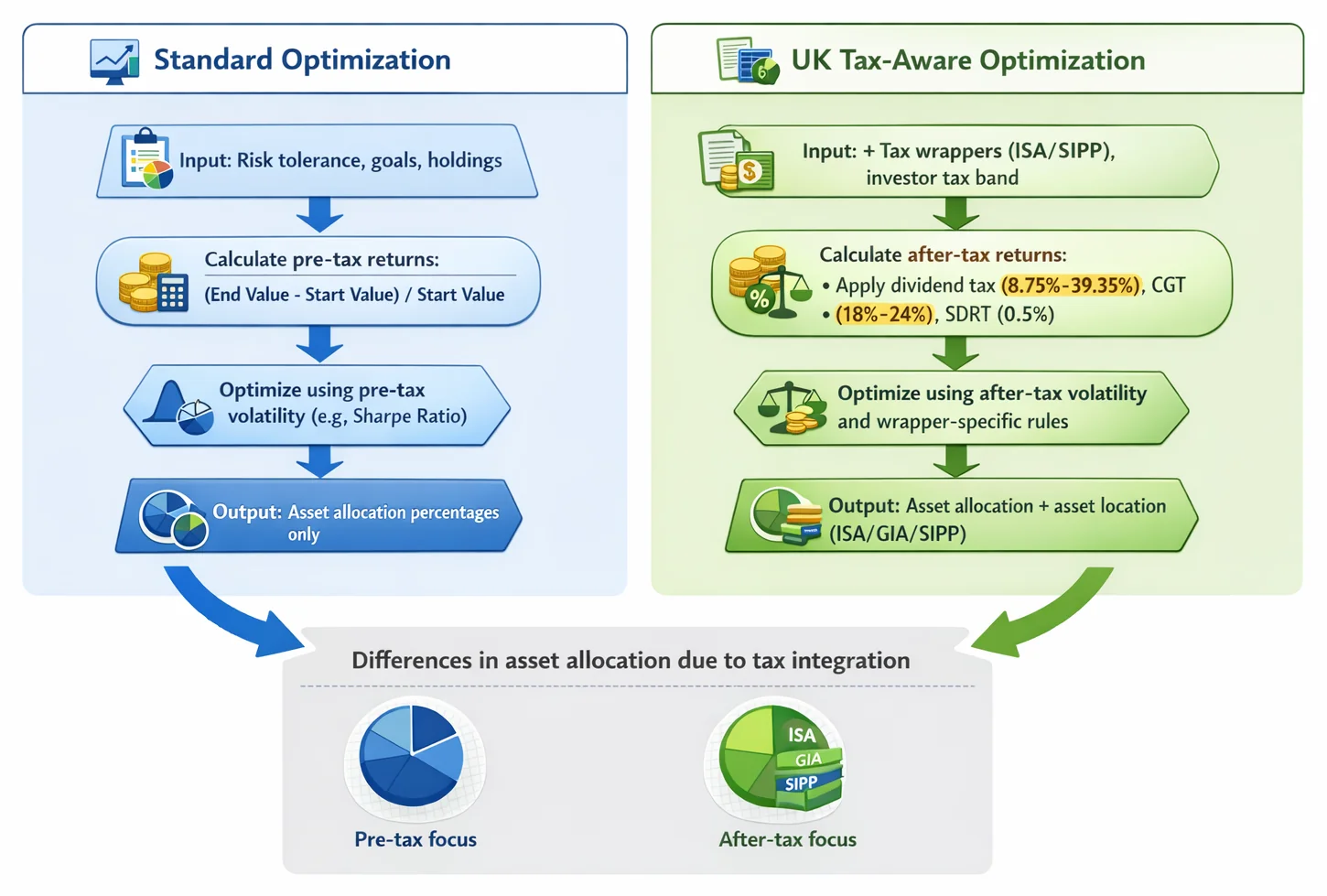

Imagine two identical portfolios with identical pre-tax returns. If held inefficiently across taxable accounts, one could deliver significantly lower after-tax income and growth due to dividend taxes, CGT liabilities, and transaction costs. Generic software won’t see this — it optimises the pre-tax numbers, potentially recommending a portfolio that’s mathematically "efficient" on paper but suboptimal in your pocket. This creates an "aha" moment: software that doesn’t integrate UK tax wrappers (like ISAs and SIPPs) and rules directly into its optimisation engine isn’t just inconvenient — it’s calculating the wrong efficient frontier. For UK investors, the most optimal tool isn’t the one with the fanciest algorithms, but the one that prioritises after-tax outcomes by default. This shifts everything — from asset location (which holdings belong in your ISA vs. GIA) to asset allocation itself. As we explore features and pricing, this tax-aware foundation becomes the paramount criterion.

How Portfolio Optimisation Works: A Step-by-Step Walkthrough

Portfolio optimisation software helps you build a smarter investment strategy by balancing risk and potential returns. Here’s how it typically works in four straightforward steps — and why UK investors need to pay special attention to a critical gap in this process.

Step 1: Input Your Details You start by telling the software key information: your risk tolerance (e.g., "I can handle moderate market swings"), financial goals ("I need £500,000 for retirement in 20 years"), and current holdings ("I own £50,000 in UK shares and bonds"). This gives the system a foundation. Some tools also ask about your time horizon or ethical preferences. The more accurate your inputs, the better the recommendations.

Step 2: Calculate Risk vs. Return

The software analyses thousands of potential portfolios using historical data and forecasts. It plots them on a graph showing risk (volatility) versus expected return. The best portfolios form the efficient frontier — a curve representing the "sweet spot" where you get the highest possible return for a chosen risk level. Returns are calculated simply: if you start with £10,000 and end with £11,000, your return is (£11,000 - £10,000) / £10,000 = 10%. Crucially, this is a pre-tax calculation. It ignores real-world costs like UK taxes, which we’ll address later. For deeper context, see our plain-English guide to the Markowitz Portfolio Optimisation method behind this.

Step 3: Algorithm Magic

Advanced algorithms — increasingly powered by AI and machine learning — crunch the data to find portfolios on the efficient frontier. They use data analytics to forecast trends, simulate market scenarios, and identify hidden patterns. Some platforms add real-time risk management, monitoring live market shifts to flag dangers like sudden stock crashes. But remember: the outputs (your ideal mix of assets) matter more than the tech wizardry. Test different scenarios using our free Portfolio Calculator.

Step 4: Output Your Ideal Allocation

The software suggests your optimal asset allocation, like "60% global stocks, 30% bonds, 10% commodities." This aims to maximise growth while staying within your risk comfort zone. You might adjust this based on fees or personal views, but the goal is a balanced, data-driven strategy. For long-term planning, factor in compounding — our Compound Interest Calculator shows how small return differences add up.

The UK Investor’s Critical Gap

This entire process focuses on pre-tax returns. For UK investors, that’s a fundamental flaw. Taxes like the 0.5% Stamp Duty Reserve Tax on UK share purchases, dividend taxes (with a £500 allowance then rates up to 39.35%), or Capital Gains Tax (with a £3,000 annual exemption and rates up to 24%) can slash your actual returns. Even basic costs matter: a portfolio returning 8% pre-tax might deliver just 5-6% after UK taxes.

Worse, tax wrappers like ISAs (with £20,000 annual allowances and tax-free growth) or SIPPs (with upfront tax relief) radically alter which assets belong where. Generic software ignores this, calculating the "optimal" portfolio using the wrong inputs — pre-tax volatility and returns. For you, the true "efficient frontier" depends on after-tax outcomes. That’s why the next section covers the non-negotiable feature UK investors need: software that bakes these rules directly into its optimisation engine.

Industry context: The global portfolio software market is growing fast — but not all tools handle UK tax nuances. Prioritise those that do.

For a practical start, explore our Free Tools to model basic portfolios, or learn how metrics like the Sharpe Ratio measure risk-adjusted performance in a UK context.

Why UK Tax Rules Shatter Generic Optimisation (The After-Tax Imperative)

Here’s the critical realisation: Portfolio optimisation software built for global markets is mathematically flawed for UK investors. Why? Because it typically maximises pre-tax returns against volatility, ignoring how UK taxes demolish those returns. The "efficient frontier" shown by generic tools becomes a theoretical mirage once HMRC takes its share. Let’s break down why:

1. ISAs: The Asset Location Imperative

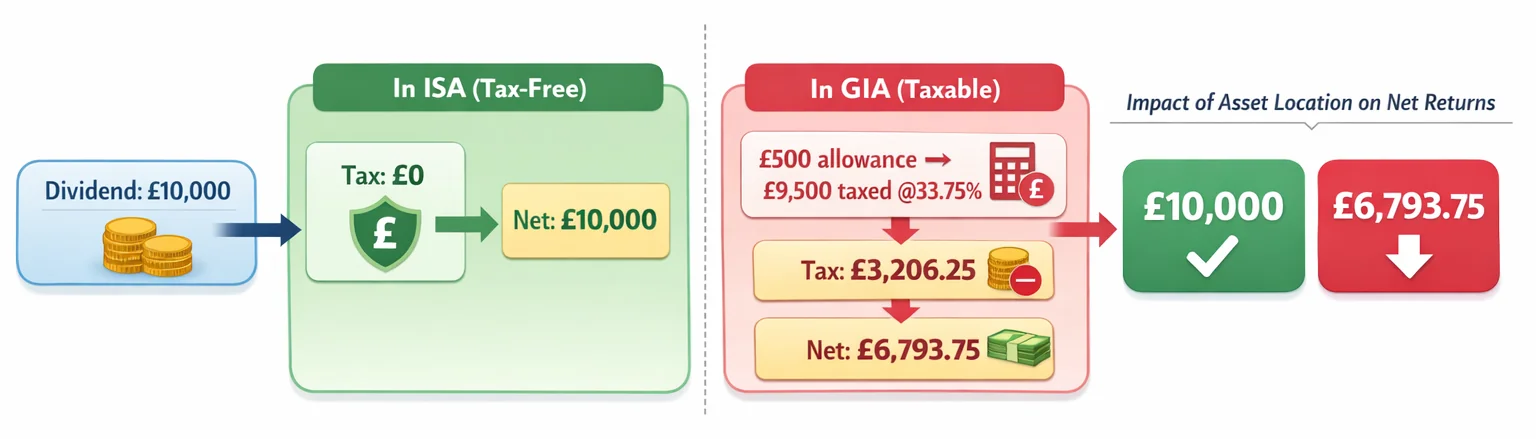

Your £20,000 annual ISA allowance isn’t just a tax wrapper — it’s a return multiplier. Consider a £10,000 dividend:

- Inside an ISA: You keep all £10,000 tax-free.

- In a taxable account: A higher-rate taxpayer pays 33.75% tax on £9,500 (after the £500 allowance), leaving just £6,793.75. Generic software won’t prioritise stuffing high-dividend assets (like UK equities) into your ISA first. But doing so can substantially boost the net return on that asset — a shift no algorithm should ignore.

2. SIPPs: The 20%+ Head Start

Pension contributions enjoy immediate tax relief. A £800 SIPP contribution becomes £1,000 instantly for basic-rate taxpayers. This means:

- Identical assets held in a SIPP start with higher effective capital.

- Growth compounds from a larger base, yet most tools treat SIPP and GIA returns identically. Without modelling this uplift, software underestimates SIPPs’ return potential and misallocates assets.

3. Dividend Tax: The Silent Return Killer

UK dividend tax has brutal tiers (8.75%/33.75%/39.35%) with a tiny £500 allowance. A "high-yield" equity fund generating 5% income delivers wildly different net returns across accounts:

- ISA/SIPP: Full 5% yield.

- Taxable account (higher-rate taxpayer): Just 3.31% after tax. Optimisation tools using pre-tax yields will overweight taxable income assets, eroding real-world returns.

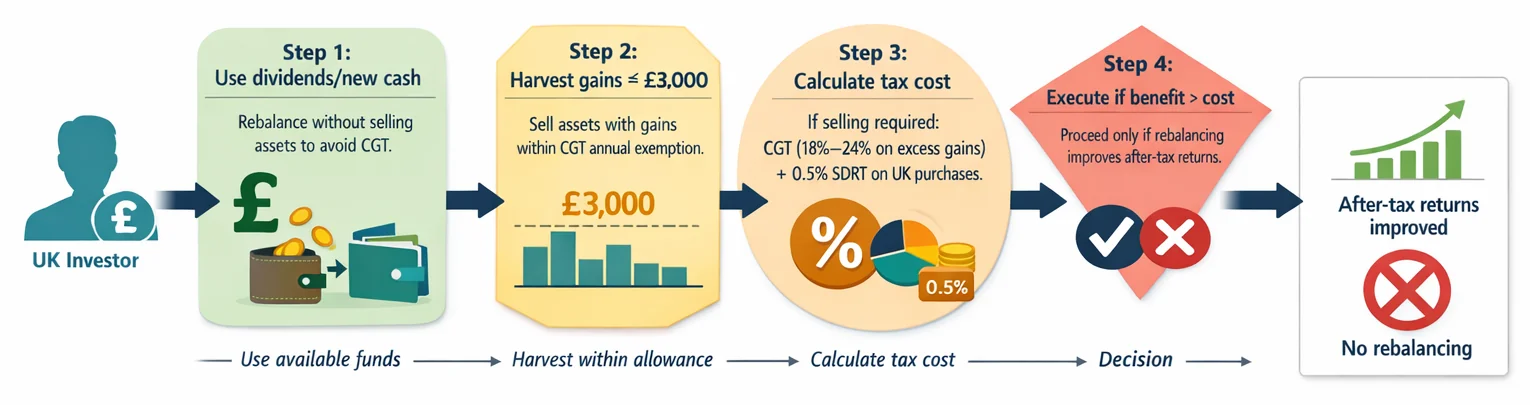

4. CGT Allowances & Rebalancing Traps

With capital gains tax at 18% or 24% and a £3,000 annual exemption, rebalancing has hidden costs. Generic software might urge selling a taxable asset with £15,000 gains to "optimise" allocation, triggering £2,880 in tax (£15,000 - £3,000 exemption × 24%). True optimisation software factors this, suggesting:

- Using dividends/new cash for rebalancing.

- Prioritising tax-free wrappers for high-turnover assets.

- Harvesting gains within allowances annually.

The Integration Gap

Superficial tax "reporting" features don’t solve this. Only software that bakes UK tax rules directly into its optimisation engine — calculating after-tax returns and risk for every asset before suggesting allocations — delivers valid results. Otherwise, you’re optimising for a fictional tax-free universe.

This tax-aware approach also enables true personalised portfolio management. Your specific tax rate (basic/higher/additional) and wrapper limits (ISA/SIPP usage) alter the maths entirely. Meanwhile, scalability becomes critical as portfolios grow: more assets mean more complex cross-wrapper tax interactions during rebalancing.

For deeper context, see our guides on the Sharpe Ratio (which should use after-tax returns) and Markowitz optimisation fundamentals. Test scenarios with our portfolio calculator to see tax’s real-world impact.

In short: If the software doesn’t treat UK tax as core to its maths, its "optimal" portfolio could leave you 20-40% poorer after tax. The efficient frontier isn’t a fixed line — it’s reshaped by every investor’s tax reality.

Key Features to Demand in UK Portfolio Optimisation Tools

For UK investors, the true measure of portfolio optimisation software lies not in complex algorithms alone, but in how effectively it handles the unique tax landscape. Generic tools optimising pre-tax returns often recommend inefficient strategies because they ignore how UK tax wrappers and rules fundamentally reshape the efficient frontier. Your software must prioritise after-tax outcomes above all else. Here’s what to demand:

- Deep UK Tax Wrapper Integration (Non-Negotiable): The tool must embed ISAs and SIPPs directly into its optimisation engine — not just track them passively. Why? Because assets held in an ISA are entirely shielded from Capital Gains Tax and dividend tax, while SIPPs offer upfront tax relief. Software that treats all accounts identically cannot optimise properly. For example, holding high-dividend UK shares outside an ISA could incur tax at 33.75% (higher rate) versus 0% inside the wrapper — a difference that drastically alters optimal allocation.

- Real After-Tax Return Calculations: Demand dynamic modelling using current UK tax rates. This means:

- Applying the 0.5% Stamp Duty Reserve Tax (SDRT) on UK share purchases.

- Calculating dividend tax using the £500 allowance (2024/25), then rates of 8.75%, 33.75%, or 39.35%.

- Factoring in Capital Gains Tax with the £3,000 annual exempt amount and rates of 18% (basic) or 24% (higher). Without this, projected "gains" are misleading. A tool showing a 7% pre-tax return might deliver under 5% after tax — making a lower-volatility, tax-efficient alternative objectively better.

- Automated Allowance Tracking: The software should proactively incorporate annual allowances into its scenarios. It must "use" your £20,000 ISA allowance optimally each year in forecasts and factor in CGT exemptions when simulating rebalancing or disposals. Manual allowance tracking invites costly oversights, like triggering avoidable CGT by not utilising the £3,000 exemption.

- Asset Location Optimisation: Beyond what to hold, the tool must recommend where to hold it (ISA, SIPP, GIA). High-growth assets? Prioritise ISAs to avoid CGT. Income-generating assets? Shelter them from dividend tax. SIPPs suit assets benefiting from long-term compounding. This feature is critical — poor asset location can erode years of returns.

Nice-to-Haves vs. Must-Haves

While features like AI-driven rebalancing sound impressive, many AI tools fall short of delivering robust, repeatable outcomes. Cloud-based access is practical for real-time updates, but it’s secondary to tax integration. Similarly, while tools like our Portfolio Calculator help model basics, true optimisation requires deeper tax-aware engines.

Pricing Justification

Higher pricing is only warranted if the software delivers on these UK-specific tax features. Paying for sophisticated risk modelling or AI predictions is futile if the tool ignores SDRT on UK shares or misrepresents dividend tax impacts. Before comparing costs, verify the core engine integrates UK rules — otherwise, you’re optimising for the wrong portfolio. For foundational concepts like the Sharpe Ratio or Markowitz optimisation, explore our guides, but remember: in the UK investing, tax integration isn’t an add-on — it’s the optimisation.

Common UK Investor Mistakes with Optimisation Software

Choosing portfolio optimisation software is a powerful step, but UK investors often stumble by overlooking how profoundly UK tax rules alter the optimisation process. Remember: the "optimal" portfolio isn't about pre-tax returns on a chart; it's about what lands in your pocket after HMRC takes its share. Here are critical pitfalls and how to avoid them:

Mistaking Tax Reporting for Tax-Aware Optimisation (The Core Error): Many platforms offer excellent compliance and reporting tools that track your capital gains or dividend income across accounts. This is useful, but it’s fundamentally different from tax-aware optimisation. The critical mistake is assuming that because the software reports on taxes, it uses tax data in its core calculations. Software that doesn’t actively factor in the 0.5% Stamp Duty Reserve Tax (SDRT) on UK share purchases, the £500 dividend allowance, the £3,000 Capital Gains Tax (CGT) annual exempt amount, or the tax-free nature of ISAs within its optimisation engine is mathematically flawed. It will prioritise pre-tax volatility and returns, potentially recommending an allocation that’s suboptimal after tax. Avoidance Strategy: Ask vendors directly: "Does your optimisation engine calculate the efficient frontier using post-tax returns and after-cost figures, including SDRT and specific UK tax rates on dividends and gains?" If they can’t confirm this deep integration, the software’s core function is misaligned with UK reality. Paying for sophisticated centralised portfolio visibility features becomes pointless if the underlying optimisation ignores tax drag.

Over-Prioritising Fancy Algorithms (Irrelevant Without Tax Integration): Analytics in portfolio management is a fast-growing field, with many tools boasting AI or complex algorithms. However, if the software isn’t built with UK tax rules hardwired into its core logic, these features are irrelevant. An AI that doesn’t understand that dividends inside an ISA are tax-free, while those in a GIA are taxed at up to 39.35%, will generate recommendations based on a fictional, pre-tax world. The fanciest algorithm is worthless if it optimises for the wrong objective. Avoidance Strategy: Prioritise "boring" tax integration over buzzwords. Test the software: Input identical assets but change their assigned wrapper (e.g., move a high-dividend stock from a GIA to an ISA). If the recommended portfolio allocation doesn’t shift significantly to favour holding income-generating assets within the ISA, the optimisation isn’t tax-aware. Don’t pay a premium for AI that ignores your £20,000 ISA allowance.

Ignoring 'Asset Location' (Beyond Just Percentages): Traditional optimisation focuses solely on asset allocation (e.g., "60% equities, 40% bonds"). For UK investors, asset location — deciding which assets go inside specific wrappers like ISAs or SIPPs — is equally crucial. Software that doesn’t model location alongside allocation misses massive opportunities. For example, holding high-growth assets subject to 24% CGT outside an ISA wastes the annual £3,000 CGT exemption and shelters less value long-term. Avoidance Strategy: Ensure the software explicitly models different account types (GIA, ISA, SIPP) and their tax treatments during optimisation. Ask: "Can your tool optimise both asset allocation percentages and the placement of specific assets across my different tax wrappers to maximise after-tax returns?" Tools like our ROI Calculator can help illustrate the long-term impact of tax drag, emphasising why location matters.

Not Updating Tax Settings (Static Rules in a Dynamic World): UK tax rules change — the dividend allowance has shrunk significantly in recent years, and CGT rates were adjusted in April 2024. Software relying on outdated assumptions (like the abolished 10% dividend tax credit) will produce incorrect optimisations. With most software now delivered via the cloud, providers have less excuse for delayed updates. Avoidance Strategy: Choose vendors committed to prompt, verified UK tax changes. Ask: "How quickly do you update your software for new HMRC rules, like changes to allowances or rates? Can I see a changelog?" Verify settings yourself annually. Relying on outdated software wastes fees and risks building a portfolio on incorrect tax assumptions, undermining the core benefit of optimisation. Understanding foundational concepts like the Markowitz Portfolio Optimisation: Plain English is helpful, but always remember: for the UK investor, tax integration isn’t a nice-to-have feature; it’s the essential lens through which true optimisation must be viewed. Choosing software without it means paying for a tool that solves the wrong problem.

Your Action Plan: Implementing UK Tax-Aware Optimisation

Now that true portfolio efficiency hinges on after-tax returns, not pre-tax metrics, it’s time to act. Generic software might plot an "efficient frontier" using volatility and raw returns, but as a UK investor, your real frontier is shaped by ISAs, SIPPs, dividend taxes, and Capital Gains Tax (CGT). Here’s how to implement optimisation that reflects your actual wealth-building potential:

- Audit Your Current Tools (Focus on the Engine): Don’t assume tax features are baked into the optimisation engine. Many tools merely add tax estimates after generating portfolios. Ask:

- Does it adjust expected returns for UK dividend tax (e.g., £500 allowance, then rates of 8.75%/33.75%/39.35%) before optimising?

- Can it model the 0.5% Stamp Duty Reserve Tax (SDRT) on share purchases when rebalancing?

- Does it prioritise harvesting the £3,000 CGT annual exempt amount within taxable accounts? If your tool treats an ISA and a taxable account identically during optimisation, it’s generating mathematically flawed results. As explored in our guide to the Sharpe Ratio, a high pre-tax risk-adjusted return can mask poor after-tax outcomes.

- Shortlist "Tax-First" Software (Scrutinise UK Integration): The global portfolio optimisation market is booming, with much of the activity concentrated in North America. This means more options exist, but many remain US-centric. Prioritise software explicitly advertising UK tax integration within the optimisation algorithm. Key features to seek:

- Asset Location Intelligence: Automatically assigns assets (e.g., high-dividend stocks, bonds) to optimal wrappers (ISA, SIPP, GIA) based on your tax band.

- Dynamic CGT & Dividend Modelling: Adjusts for your personal allowances and rates during scenario testing.

- SDRT Costing: Factors in the 0.5% transaction tax on UK share purchases. Tools like predictive analytics are only valuable if they forecast after-tax outcomes under UK rules.

- Use Free Trials (Test Critical UK Scenarios): Don’t rely on marketing claims. During trials, run these tests:

- ISA vs. GIA Impact: Optimise the same portfolio twice-once assuming all assets are in an ISA (tax-free), once in a General Investment Account (taxable). Does the "optimal" asset allocation change significantly? It should.

- Dividend Drag Test: Input a portfolio heavy in UK equities. Does the software reduce exposure in taxable accounts once your £500 dividend allowance is exceeded, shifting to growth stocks or ISA holdings?

- Rebalancing Cost Check: Simulate selling £5,000 of UK shares in a GIA. Does the output account for CGT (£3,000 allowance, then 18% or 24%) and SDRT on repurchases? Use our ROI Calculator to manually verify after-tax outcomes from the software’s suggestions.

Start Simple (Optimise Your ISA First): ISAs offer the cleanest starting point: no CGT, no dividend tax. Use your software to optimise within your £20,000 annual ISA allowance. This simplifies resource optimisation by isolating tax-free growth. Once satisfied, layer in taxable accounts and SIPPs (factoring in pension tax relief). This phased approach builds confidence and highlights how tax wrappers alter asset allocation.

Schedule Tax-Check Reviews (Post-Budget Essential): UK tax rules evolve (e.g., CGT allowance falling to £3,000 in 2024/25). Schedule quarterly reviews and a mandatory check after the Autumn Budget. Verify your software updates its tax parameters promptly. A tool that lags on tax changes invalidates its own optimisations.

Why This Transforms Your Wealth Building: Prioritising deep tax integration shifts portfolio optimisation from an academic exercise to a practical engine for compounding wealth. Imagine two identical portfolios returning 7% annually. If one suffers a 1.5% annual tax drag due to inefficient asset location, the gap over 20 years on a £100,000 investment runs to tens of thousands of pounds. Software that bakes in UK rules — like ARIA PM, which handles survivorship adjustment, cost modelling, and regime stress-testing automatically — lets you focus on strategy, not manual calculations. As the industry shifts towards more personalised solutions, demand tools that personalise for UK tax. By anchoring your optimisation in after-tax reality, you turn theory into tangible financial advantage. For foundational concepts, revisit Markowitz Portfolio Optimisation: Plain English and explore our Free Tools to test correlations and costs.

Key Takeaways

- Prioritise portfolio optimisation software that integrates UK tax wrappers (ISAs, SIPPs) and dividend/capital gains rules directly within its calculation engine to maximise your actual after-tax returns.

- Ensure the software calculates the efficient frontier using your after-tax returns, not misleading pre-tax metrics like the Sharpe ratio, as UK tax significantly alters net outcomes.

- Verify the software automatically factors in specific UK tax rules like the £500 dividend allowance, £3,000 capital gains tax exempt amount, and differing dividend/capital gains tax rates.

- Reject software treating UK tax wrappers as mere reporting features; their impact on asset location and allocation must be core to the optimisation algorithm itself.

- Justify higher software pricing only if it delivers this deep UK tax integration, making it the primary selection criterion over generic optimisation features.

How UK Tax Rules Transform Portfolio Optimisation: Pre-Tax vs. After-Tax

| Feature | Generic (Pre-Tax) Optimisation | UK Tax-Aware Optimisation |

|---|---|---|

| Primary Goal | Maximises pre-tax returns for given volatility | Maximises after-tax returns accounting for UK tax liabilities |

| Tax Wrapper Handling | Treats ISAs/SIPPs as generic accounts | Actively optimises asset location within wrappers based on tax efficiency |

| Dividend Treatment | Uses gross dividend yields | Adjusts for dividend tax rates (0%, 8.75%, 33.75%, 39.35%) |

| Capital Gains Impact | Ignores CGT implications during rebalancing | Factors in CGT allowances (£3,000 in 2024/25) and tax rates |

| Efficient Frontier | Based purely on risk-return tradeoff | Redefined by after-tax returns and net volatility |

| UK Suitability | Mathematically flawed for UK investors | Generates truly optimal UK-specific portfolios |

Must-Have Features for True UK Tax-Aware Optimisation

| Critical Feature | Why It Matters | Consequence If Missing |

|---|---|---|

| Deep Engine Integration | UK tax rules directly drive optimisation calculations | Tax becomes an afterthought, leading to suboptimal asset allocation |

| Dynamic ISA/SIPP Modelling | Optimises asset location across wrappers in real-time | Missed tax-free growth opportunities and contribution inefficiencies |

| Dividend Tax Band Adjustment | Personalises optimisation based on investor's tax band | Over/under-exposure to dividend stocks, reducing net returns |

| CGT Harvesting Logic | Automates gain/loss timing within allowances | Higher tax bills and inefficient use of the £3,000 annual exemption |

| Tax Year Synchronisation | Aligns rebalancing with April allowance resets | Wasted allowances and unnecessary tax liabilities |

Sources

- FCA InvestSmart: Is it the right investment for you? — FCA guidance on assessing whether an investment platform or product fits your needs, covering costs, risk, and regulatory checks.

- MoneyHelper: Investing — UK government-backed advice hub on investing, including platform charges and suitability considerations.

- FCA: Automated investment services — our expectations — Regulatory guidance on robo-advisors and automated portfolio tools, including key risks and benefits.

- Investopedia: Portfolio Management — Foundational concepts of portfolio optimisation, diversification, and risk-return trade-offs.

- SEC: Investor Bulletin — Automated Investment Tools — SEC guidance on the benefits, limitations, and key features of automated investment tools.

- CFA Institute: Portfolio Management — Practitioner-level resources on portfolio construction theories and optimisation techniques (membership required for full access).