You've carefully built a diversified ISA or SIPP portfolio, but over time, some investments surge while others lag, throwing your carefully planned asset allocation off track. Manually correcting this "drift" feels complex and time-consuming, and you worry selling winners might trigger unwanted tax bills. This inefficiency isn't just inconvenient; it risks undermining your long-term returns and missing out on the powerful tax advantages uniquely offered by UK ISAs and SIPPs. This article explains how Portfolio Rebalancing Software for UK ISA and SIPP Investors transforms this chore. You'll discover it's far more than simple maths — it's a sophisticated tool that systematically exploits the tax-free status of these wrappers. By algorithmically harvesting gains and losses without incurring Capital Gains Tax, this software acts as a hidden compounding engine, accelerating wealth growth in ways manual methods simply cannot match.

What Portfolio Rebalancing Software Actually Does (And Why It's Not Just Math)

This is where portfolio rebalancing software steps in. At its core, it's a digital tool designed to automate the process of adjusting your investments back to your predetermined target allocations. You set your desired mix (e.g., 50% global stocks, 30% bonds, 20% alternatives), and the software continuously monitors your holdings. When drift exceeds a threshold you define (say, 5%), it calculates the precise trades needed — which assets to sell and which to buy — to restore your portfolio to its target state. It’s far more than a simple calculator; it’s a sophisticated, rules-based system managing a complex optimisation problem.

Contrast this with manual rebalancing. Calculating trades across multiple holdings within accounts like your ISA or SIPP, while factoring in transaction costs like the 0.5% Stamp Duty Reserve Tax (SDRT) on UK share purchases, is complex and time-consuming. Manual methods are also error-prone: it is easy to miscalculate the trades needed. This could mean selling too much of a winning asset (missing future gains) or buying too little of an underperformer (failing to capitalise on potential recovery), silently eroding your long-term compound growth. Software eliminates this human error factor, executing the rebalancing algorithm with precision and speed.

But the true power for UK investors, especially within the tax-sheltered environments of an ISA or SIPP, goes far beyond mere arithmetic accuracy and convenience. While maintaining your target risk level (crucial for long-term strategies grounded in principles like the Sharpe Ratio) is vital, the software’s algorithmic nature unlocks a hidden advantage: it systematically harvests gains and losses within these wrappers in the most tax-advantaged way possible. Because gains and dividends inside an ISA are entirely tax-free, and SIPPs offer significant sheltering (though with different tax rules on withdrawal), the software can constantly nudge your portfolio back to target without ever triggering a Capital Gains Tax (CGT) bill that would erode your returns in a taxable account. This transforms rebalancing from a simple maintenance chore into a powerful, automated engine for tax-advantaged compounding. By consistently selling high (within the wrapper) and buying low, free from the drag of CGT on each rebalance, the software accelerates wealth growth in a manner fundamentally impossible through manual intervention or within a standard taxable brokerage. Understanding the underlying portfolio optimisation principles, as explained in our guide to Markowitz Portfolio Optimisation, helps appreciate why this systematic approach is so effective. The cumulative effect over years, amplified by compound interest, can be substantial, turning disciplined rebalancing into a significant driver of net returns.

The ISA/SIPP Advantage: How Rebalancing Software Becomes a Tax-Free Compounding Machine

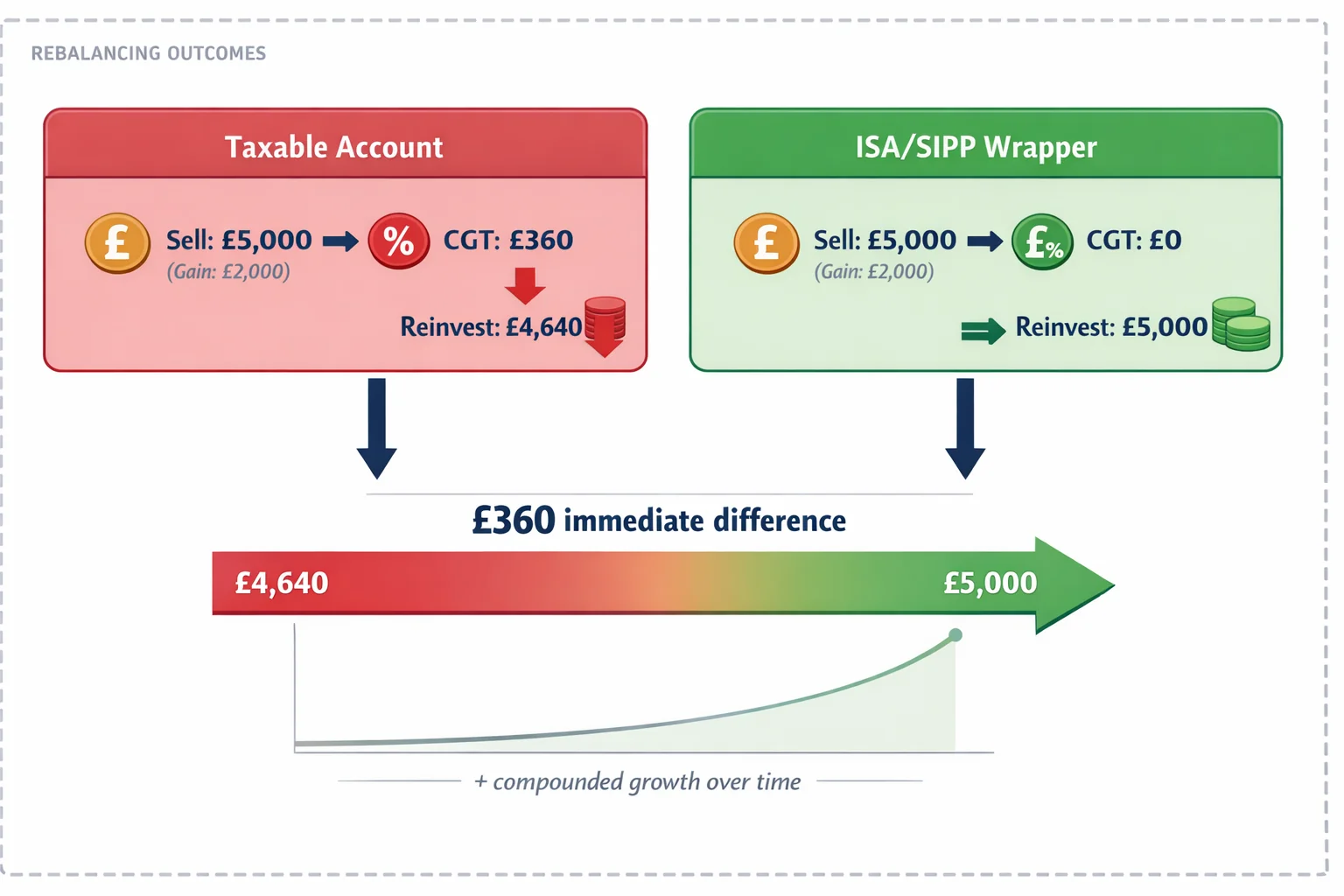

For UK investors using ISAs and SIPPs, portfolio rebalancing software isn't just a maintenance tool — it's a hidden engine for accelerated wealth growth. The secret lies in exploiting the unique tax mechanics of these wrappers. Unlike taxable accounts, where selling assets to rebalance can trigger Capital Gains Tax (CGT) — currently 18% or 24% on gains above the £3,000 annual exempt amount — trades within ISAs and SIPPs incur zero CGT. This transforms rebalancing from a necessary chore into a powerful, tax-free wealth-building strategy.

Here’s how it works: When markets shift, certain assets outperform while others lag. Rebalancing software algorithmically "harvests" gains from winners and redirects capital to underperformers — effectively buying low and selling high. In a taxable account, selling winners would incur an immediate CGT penalty, eroding capital and discouraging timely adjustments. But inside an ISA or SIPP, this entire process happens tax-free. Every pound from sold assets is fully reinvested, maximising exposure to potential rebounds in undervalued holdings. This tax efficiency is transformative. Consider a simple example: Selling £5,000 of an overperforming stock with £2,000 in gains. In a taxable account, a basic-rate taxpayer would pay £360 in CGT (18% of £2,000), leaving only £4,640 to reinvest. In an ISA or SIPP, the full £5,000 is redeployed. Over decades, avoiding such leaks allows compounding effect to work unimpeded. Even a 0.5% annual improvement in returns — achievable through consistent, tax-free rebalancing — can mean tens of thousands more in your portfolio over 20 years. Our Compound Interest Calculator vividly illustrates how small advantages snowball.

The automation aspect is crucial. Manual rebalancing is time-consuming and emotionally fraught, often leading to delays or missed opportunities. Software executes this systematically, using predefined rules or AI-driven analytics to optimise timing and thresholds. Cloud-based platforms ensure this happens efficiently, scaling with your portfolio and providing real-time insights from any device. Adoption of these tools among self-directed investors has been growing steadily.

Contrast this with taxable investing, where CGT creates a "tax drag" that stifles proactive management. Investors often hold winners too long to defer taxes or avoid selling losers to dodge realising losses — both of which increase risk and reduce returns. Tax wrappers remove this friction entirely. By pairing them with automated rebalancing, you systematically enforce discipline, maintain your target risk level (as defined by frameworks like Markowitz Portfolio Optimisation), and potentially enhance your Sharpe Ratio — all while shielding gains from the taxman.

In essence, portfolio rebalancing tools for ISAs and SIPPs turn tax efficiency into a compounding superpower. They ensure your money works harder, longer, and entirely for you — making them indispensable for building wealth efficiently within the UK’s most popular tax wrappers. For a deeper dive into long-term growth projections, explore our Investment Calculator.

Step-by-Step: How Rebalancing Software Works for Your UK Portfolio

Portfolio rebalancing software transforms a tedious manual task into an automated, tax-efficient engine — particularly powerful within UK ISAs and SIPPs. Here’s how it operates in practice:

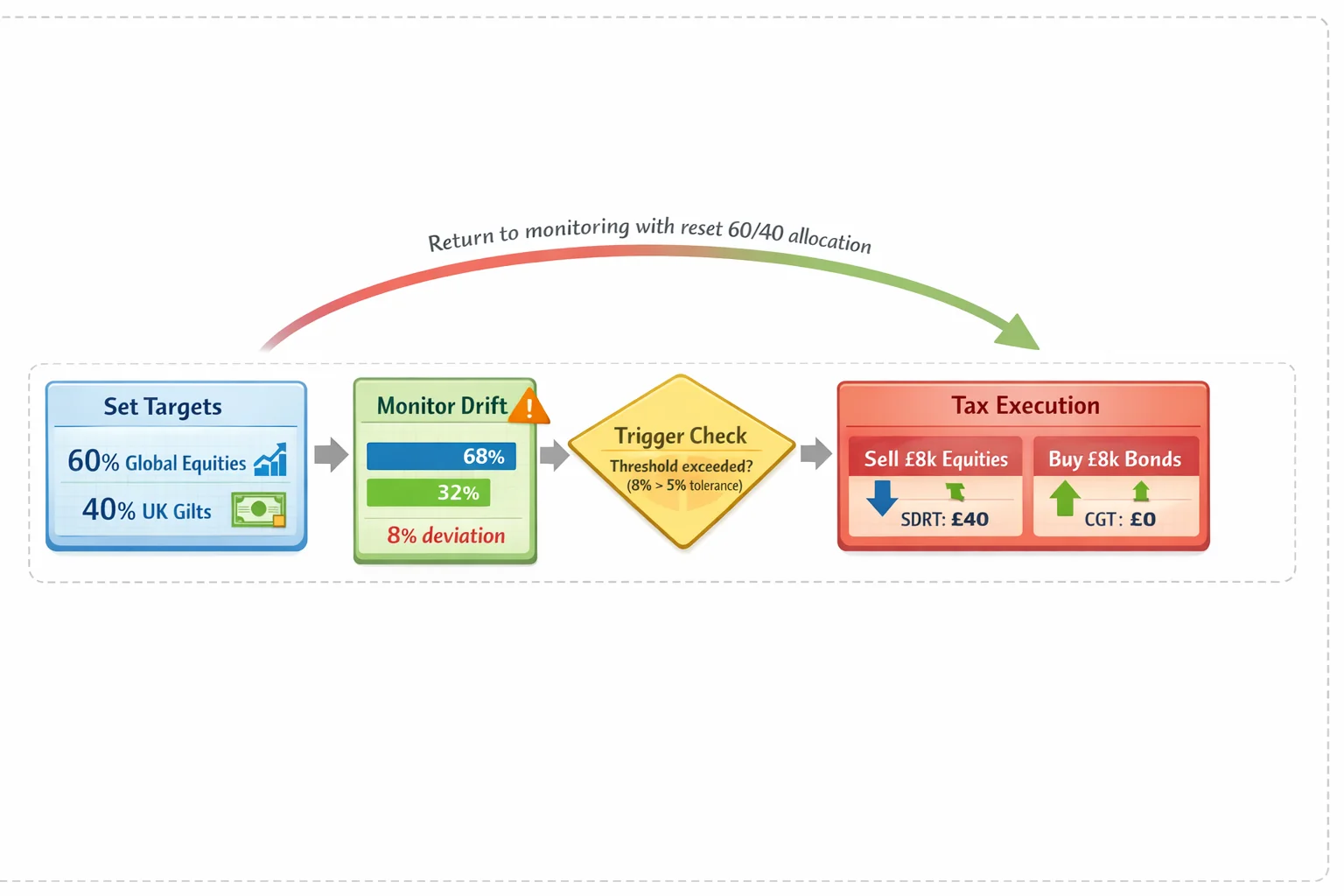

Set Your Target Allocations You begin by defining your ideal asset mix — for example, 60% global equities and 40% UK government bonds. This target reflects your risk tolerance and goals, informed by principles like Modern Portfolio Theory (explained in our guide to Markowitz Portfolio Optimisation). The software stores these targets as its baseline.

Continuous Monitoring for Drift Using investment tracking tools, the software scans your portfolio in real-time. It compares your actual holdings against your targets, accounting for market movements, dividends, and deposits. For instance, if equities surge to 68% of your portfolio while bonds drop to 32%, the system flags this imbalance.

Threshold or Calendar Triggers Rebalancing activates in two ways:

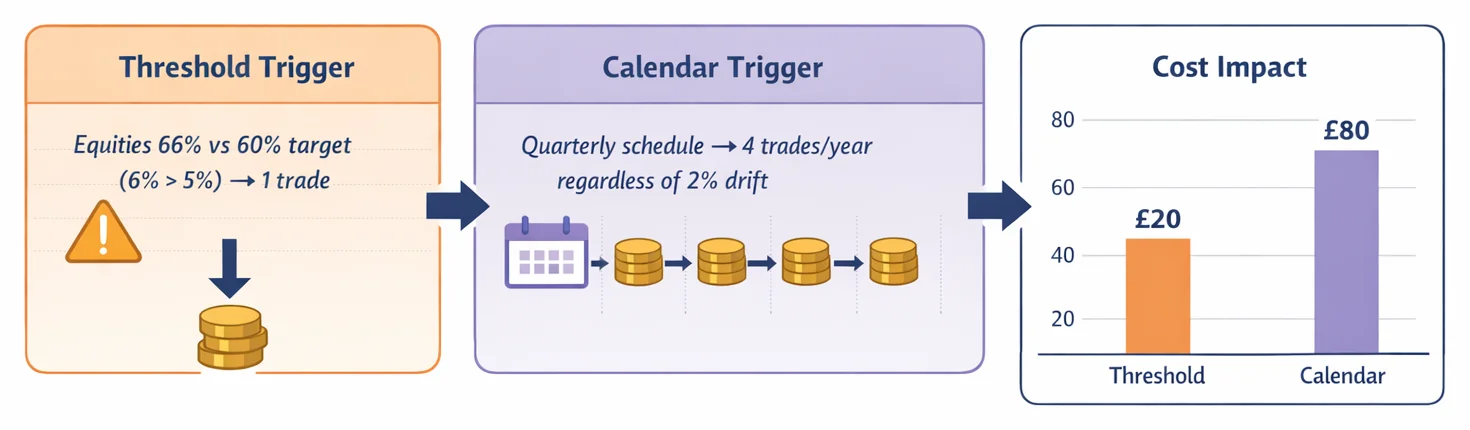

- Threshold-based: Trades trigger when an asset deviates by a set margin (e.g., 5% from target). This method captures market opportunities faster.

- Calendar-based: Rebalancing occurs at fixed intervals (e.g., quarterly). Many investors and advisers prefer to give final approval before trades execute. To accommodate this, most tools offer a ‘review mode’ — sending you an action plan to approve or adjust.

- Tax-Optimised Execution Crucially, trades occur inside your ISA or SIPP. Since these wrappers shield gains from Capital Gains Tax (CGT) and dividend tax, the software:

- Sells overweight assets (e.g., equities) and buys underweight ones (e.g., bonds) with zero CGT liability.

- Incurs unavoidable costs like Stamp Duty Reserve Tax (SDRT) at 0.5% on UK share purchases — but avoids external tax penalties. This tax-free recycling turns rebalancing into a compounding accelerator. For example, £10,000 growing at 7% annually for 20 years becomes £38,697. With a 0.5% annual drag from manual inefficiency, it drops to £35,000 — a £3,697 difference. Test scenarios yourself with our Compound Interest Calculator.

Integration & Efficiency Leading tools sync with UK platforms like Hargreaves Lansdown or AJ Bell, automating data feeds. Cloud-based systems enable instant calculations, reducing human error. This automation can meaningfully lower rebalancing costs through optimised trade sizing and timing.

Beyond Rebalancing: Performance Insights Post-trade, performance analysis tools benchmark returns against indices like the FTSE 100. You’ll assess metrics like risk-adjusted returns, clarified in our Sharpe Ratio guide.

By automating rebalancing within tax shelters, this software systematically harvests gains, sidesteps CGT, and compounds growth relentlessly. For deeper strategy testing, tools like ARIA PM handle survivorship bias and cost modelling automatically — letting you focus on outcomes.

Real Tools for UK Investors: Comparing Top Rebalancing Platforms

For UK investors, choosing the right portfolio rebalancing software is critical to unlocking the compounding power of ISAs and SIPPs. These tax wrappers eliminate capital gains tax (CGT) on trades, turning rebalancing into a tax-efficient engine for growth. As portfolio management software has matured and adopted more automation, these tools have become smarter and more accessible than ever. But options vary widely in automation, cost, and ISA/SIPP integration. Here’s how top UK-accessible solutions compare.

Robo-Advisors (e.g., Nutmeg, Moneyfarm) offer fully automated rebalancing. They build and manage your entire ISA or SIPP portfolio, using algorithms to maintain your target allocation. For example, after a market rally shifts a £50k ISA to 70% equities against a 60% target, they’ll automatically sell shares and buy bonds to restore balance — all without triggering CGT inside the wrapper. Costs are typically charged as an annual percentage of assets under management (AUM). These platforms use risk modelling enhanced by AI, adjusting for volatility and your risk profile. However, you cede control: they select all investments and handle execution.

Broker Tools (e.g., Interactive Investor’s Portfolio Planner, AJ Bell’s Rebalancer) provide semi-automation. They generate a custom trade list to align your self-managed ISA or SIPP with your desired allocation but require manual execution. For the same £50k ISA rebalance, they’ll specify which equities to sell and bonds to buy, often optimising for trade generation to minimise costs like the 0.5% Stamp Duty Reserve Tax (SDRT) on UK share purchases. Platform fees apply (typically a flat monthly or annual account charge), plus trading commissions. Most investors using these tools prefer to keep oversight, reviewing and approving the suggested trades before they execute rather than handing full control to the algorithm. These tools suit hands-on investors but lack full automation.

Third-Party Software (e.g., Sharesight, Portfolio Visualizer) delivers advanced analytics for self-directed investors. They integrate with your existing broker to offer sophisticated risk modelling (like stress-testing against market crashes) and optimised trade lists that reduce transaction taxes. For instance, such tools can bundle trades to lower SDRT impact. Cloud-based analytics tools like these have become widely adopted for their flexibility. Costs are typically subscription-based, ranging from a free tier to a premium monthly or annual plan. Tools like ARIA PM handle survivorship adjustment, cost modelling, and regime stress-testing automatically — so you can focus on interpreting results rather than building the simulation. Most support ISA/SIPP accounts but may require manual trade execution.

Crucial Considerations: Not all platforms support auto-rebalancing — always verify if a tool executes trades or just suggests them. In our £50k ISA example, automated selling of overperforming equities avoids CGT entirely, systematically harvesting gains. This tax advantage, combined with disciplined rebalancing, compounds returns. Use our Compound Interest Calculator to model how small efficiency gains amplify over time. For deeper insights, explore risk-adjusted metrics or the foundations of modern portfolio theory. Ultimately, the right tool turns rebalancing from routine maintenance into a strategic accelerator for your UK tax wrappers.

Costly Mistakes to Avoid With Rebalancing Software

While portfolio rebalancing software can act as a powerful tax-advantaged compounding engine for UK ISA and SIPP investors, missteps can erode its benefits. Here are five critical errors to sidestep — and how to counter them:

Over-Rebalancing (Triggering Unnecessary Fees) Rebalancing too frequently — such as monthly — can rack up trading costs that compound against you. Each UK share purchase incurs Stamp Duty Reserve Tax (SDRT) at 0.5%, and brokers charge per-trade fees. For example, £10,000 in trades annually at 0.5% SDRT plus £10 broker fees would cost £60/year. Over 20 years at 7% growth, that’s £2,500+ in lost compounding. Solution: Use threshold-based triggers (e.g., 5-10% bands) instead of calendar dates. This minimises trades while keeping allocations aligned. Tools like our Portfolio Calculator model these cost impacts.

Ignoring Transaction Costs in Settings If your software assumes trades are "free," it might recommend unnecessary adjustments. Real-world costs like SDRT and broker fees must be inputted to avoid false precision. Manual rebalancing is prone to calculation slips — automated tools reduce this, but only if configured truthfully. Solution: Input actual fees and taxes during setup. Verify if the tool auto-calculates SDRT for UK shares.

Set-and-Forget Allocations Without Life Changes Your risk tolerance isn’t static. A 30-year-old’s 90% equity allocation may be disastrous at 60. Yet many investors never adjust their strategy after initial setup, missing critical life milestones. Solution: Review allocations annually or after major events (job change, inheritance). Use personalised planning tools to stress-test goals.

Triggering Avoidable CGT in Taxable Accounts Rebalancing outside ISAs/SIPPs risks Capital Gains Tax (CGT) at 18-24% on profits above your £3,000 annual exemption. This defeats the core advantage: ISA/SIPP gains are entirely tax-free. Realising a £2,000 gain above your allowance in a taxable account could cost £360–£480 in CGT (18%–24%) — a permanent drag. Solution: Verify all trades stay within tax wrappers. Prioritise rebalancing inside ISAs/SIPPs first. Never let software "harvest losses" in a wrapper — it’s unnecessary since gains aren’t taxed.

Not Setting Buffer Zones (5-10% Thresholds) Without tolerance band, software might trigger trades for tiny deviations — like a 1% equity drift. This wastes fees and attention. Solution: Apply 5-10% rebalancing thresholds. A 60% equity target wouldn’t rebalance until hitting 55% or 65%. This exploits natural market drift while cutting costs. Our correlation calculator helps identify stable assets needing fewer adjustments.

AI-driven tools are increasingly common, and algorithms now handle much of institutional rebalancing. But automation isn’t infallible. Always understand why behind trades — like how Markowitz optimisation balances risk-return — rather than blindly trusting outputs. Pair smart software settings with annual human oversight to transform rebalancing into your silent compounding ally.

Your 2026 Action Plan: Implementing Rebalancing Software

With market volatility in 2025 likely creating significant portfolio drift in your ISA and SIPP holdings, 2026 is the year to harness automation. This isn't just tidying up; it's strategically using your tax wrappers as compounding engines. Here’s your practical five-step plan:

- Audit Your Current ISA/SIPP Allocations: Start by getting a clear picture. Log into all your platforms and list every holding, its current value, and its percentage of the total ISA/SIPP portfolio. Don't rely on memory. This baseline reveals your actual portfolio drift correction needs. Tools like our Portfolio Calculator can help aggregate this data visually. Notice how far each asset class (e.g., UK equities, global bonds, specific sectors) has strayed from your intended mix.

- Define Your Target Portfolio (Risk-Aligned): What should your allocation look like? Base this on your risk tolerance and long-term goals, not last year's winners. If you haven't defined this formally, now is crucial. Consider core principles like diversification explored in our guide on Markowitz Portfolio Optimisation: Plain English. Be specific: "60% Global Equity ETF, 30% UK Gilts, 10% Gold ETC" is actionable; "mostly shares, some bonds" is not. This target is your rebalancing compass.

- Research Tools — Prioritise UK Tax-Wrapper Integration: This is critical. Not all portfolio rebalancing software understands the unique rules of ISAs and SIPPs. Look explicitly for features confirming seamless handling within these wrappers. The software must recognise that trades inside your ISA or SIPP incur the 0.5% Stamp Duty Reserve Tax (SDRT) on UK share purchases, but crucially, that selling assets within these wrappers does not trigger Capital Gains Tax (CGT). This tax-free environment is where the compounding magic happens. Adoption of such tools among individual investors has been growing rapidly, driven by the need for precision. Ensure the tool can model trades accurately across your specific ISA and SIPP accounts.

- Start with 'Alert-Only' Mode if Nervous: Jumping straight to auto-trading can feel daunting. Most quality portfolio rebalancing tools offer an 'alert-only' function. Set your drift thresholds (e.g., alert me if any asset class moves +/- 5% from target). This gives you control, reduces the fear of the unknown, and significantly cuts down error reduction in rebalancing compared to manual spreadsheets (where mistakes are common). Even these basic alerts prevent small drifts from becoming major, costly deviations. Use this mode to build confidence in the software's calculations before enabling trades.

- Schedule Quarterly Reviews: Set calendar reminders to review your portfolio and the software's performance every three months. Check the alerts generated trade suggestions, and the rationale. Did the software efficiently harvest gains from winners within your ISA tax-free environment and reinvest into underweight assets? Did it avoid unnecessary trades that would incur SDRT? Use this time to reassess if your target allocation still matches your goals, perhaps using our ROI Calculator to project different scenarios. Quarterly strikes a balance between staying disciplined and avoiding over-trading.

Start Small, Start Now: You don't need to automate everything immediately. Setting up simple drift alerts is a powerful first step that requires minimal commitment but delivers immediate value by keeping you aware. Remember, the core advantage of using portfolio rebalancing software within your ISA and SIPP is the ability to systematically buy low and sell high without the drag of CGT. Every time the software executes a tax-free rebalance within your wrapper, capturing gains or harvesting losses for reinvestment, it compounds your growth advantage exponentially over time. This transforms routine maintenance into a hidden engine for accelerated wealth building. Explore how ARIA PM handles the complexities of UK tax wrappers and portfolio drift correction to focus on strategy.

Key Takeaways

- Portfolio rebalancing software leverages the tax-free/SDRT-free environment of your ISA and SIPP to systematically harvest gains and losses algorithmically, avoiding Capital Gains Tax and boosting compound growth beyond simple allocation maintenance.

- Automated software removes the calculation errors inherent in manual rebalancing, ensuring you sell the right amount of winners and buy the correct amount of underperformers to capture potential recovery.

- The software precisely factors in transaction costs like Stamp Duty Reserve Tax (SDRT) on UK share purchases within its trade calculations, optimising execution cost-efficiency within your tax wrappers.

- Algorithmic rebalancing within your ISA or SIPP consistently maintains your target risk profile (e.g., Sharpe Ratio) by correcting drift, crucial for long-term strategy adherence without emotional bias.

- By automating complex trade calculations across multiple holdings within your ISA and SIPP, the software saves significant time and removes the hassle of manual intervention.

| Feature | Manual Rebalancing | Automated Rebalancing Software |

|---|---|---|

| Tax Efficiency | May avoid selling winners due to CGT concerns in taxable accounts; no CGT in ISA/SIPP but behavioural barriers remain | Systematically harvests gains/losses within ISA/SIPP wrappers with zero CGT implications |

| Frequency & Timing | Infrequent (often annually), allowing significant drift | Precise threshold/calendar triggers (e.g. quarterly) prevent drift |

| Emotional Bias | Prone to hesitation ("let winners run") or overtrading | Algorithmic discipline enforces targets without emotion |

| Time Commitment | Hours of analysis/trading per rebalance | Fully automated after initial setup |

| Compounding Benefit | Missed rebalancing opportunities erode long-term growth | Continuous tax-free compounding through systematic allocation maintenance |

Table 2: UK Rebalancing Software Comparison

| Platform | ISA/SIPP Integration | Tax Efficiency Features | Cost Structure | Unique Advantage |

|---|---|---|---|---|

| Nutmeg | Full native support | Auto-rebalancing within wrapper | AUM-based annual fee | All-in-one robo-advisor platform |

| Vanguard UK | SIPP/ISA compatible | CGT-free rebalancing, dividend recycling | Fund-based charges | Low-cost index fund integration |

| Interactive Investor | ISA/SIPP accounts | Custom threshold alerts, tax-wrapper optimisation | Flat monthly fee | Flexible for multi-asset portfolios |

| Wealthify | Dedicated ISA/SIPP | Auto-rebalancing with tax-wrapper awareness | AUM-based annual fee | Goal-based rebalancing strategies |

| Fidelity UK | Full wrapper support | Dividend auto-reinvestment + rebalancing | Tiered % fee | Advanced institutional-grade tools |

Sources

- FCA: Automated investment services — FCA guidance on robo-advice platforms, which typically include portfolio rebalancing features.

- MoneyHelper: Investing — UK government-backed guidance hub on investing and managing portfolios such as ISAs and SIPPs.

- Hargreaves Lansdown: Portfolio Rebalancing — Official documentation from a major UK platform explaining their rebalancing tools for ISAs/SIPPs.

- Vanguard UK: Managed Stocks and Shares ISA — Vanguard's managed ISA service, which handles portfolio rebalancing automatically for UK investors.

- Boring Money: Online Investment Platforms — Independent comparison of UK platforms, evaluating rebalancing tools and ISA/SIPP functionality.