Your annual portfolio rebalancing feels straightforward: sell overweight assets, buy underweight ones. But as a UK investor, did you realise the order of those trades could trigger unnecessary capital gains tax? This hidden inefficiency silently erodes your returns year after year. A basic Portfolio Rebalancing Spreadsheet solves the rebalancing maths, but its true power for UK savers lies elsewhere: automating tax-efficient trade sequencing. This free Excel template transforms routine maintenance into a potent tax-efficiency engine, strategically using allowances and minimising taxable gains. This article shows you how to use the template, avoiding costly mistakes. You'll learn practical steps to rebalance smarter, keeping more of your investment growth legally sheltered from HMRC. No technical expertise needed — just follow the guide.

What is Portfolio Rebalancing? (And Why Your Spreadsheet is More Than Maths)

Picture this: you carefully build an investment portfolio, allocating specific percentages to UK equities, global funds, and bonds. Fast forward a year. Your UK shares have surged, while bonds lagged. Suddenly, your carefully planned 60% equity allocation has ballooned to 75%, significantly increasing your portfolio's risk profile. This drift happens constantly due to differing market performance. Portfolio rebalancing is the essential process of buying and selling assets to bring your portfolio back in line with your original target allocations. It’s fundamental risk management, ensuring your investments don't stray too far from your intended strategy and risk tolerance.

While the core concept is simple — calculate the difference between your current holdings and your targets, then trade to close the gap — the how is where things get critical, especially for UK investors. The true power of this free Excel template isn't just in performing the rebalancing maths. Its unique value lies in automating UK tax-efficient trade sequencing — transforming routine portfolio maintenance into a hidden engine for minimising Capital Gains Tax (CGT).

Here's the challenge: every sale of an asset outside of a tax wrapper like an ISA potentially triggers a CGT liability. The UK's annual CGT exempt amount is £3,000 (2024/25), with gains above this taxed at 18% (basic rate) or 24% (higher rate). Also, buying UK shares incurs a flat 0.5% Stamp Duty Reserve Tax (SDRT). A naive rebalancing approach — simply selling winners to buy underperformers — can generate unnecessary tax bills and transaction costs. This complexity is a major reason many investors avoid rebalancing regularly; the perceived tax and cost hurdles feel too high.

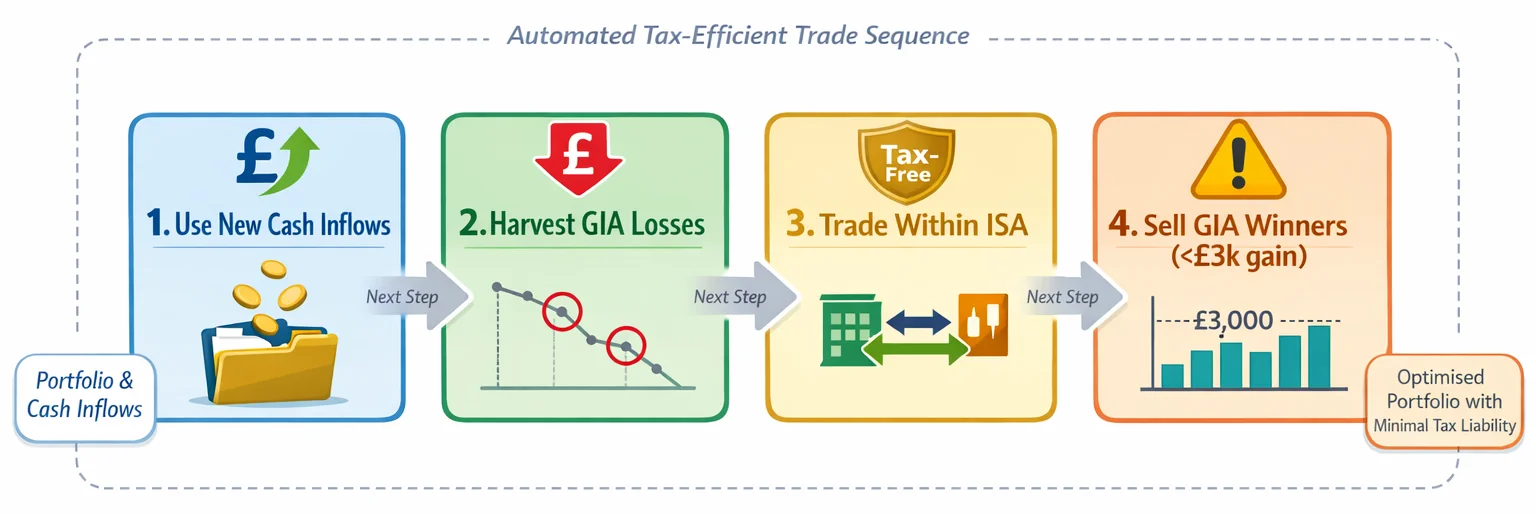

This is where the template shifts from calculator to strategist. Instead of just telling you what to buy and sell, it intelligently sequences the trades to prioritise tax efficiency. It might suggest:

- Using new cash inflows: Directing any fresh deposits (like monthly savings) towards underweight assets first, avoiding sales and thus CGT.

- Harvesting losses: Identifying assets held at a loss to sell first, using these losses to offset any unavoidable gains elsewhere in the portfolio within the same tax year.

- Minimising SDRT: Structuring buy orders efficiently, potentially prioritising assets not subject to SDRT (like non-UK shares or funds) where possible within your strategy.

- Protecting ISA allowances: Ensuring trades within your ISA (£20,000 annual allowance) are maximised, as gains and dividends here are completely tax-free.

By automating this complex sequencing logic, the template tackles the primary barrier to regular rebalancing: the fear of triggering tax. It ensures you're not just maintaining your target allocation — crucial for managing risk as explained in our guide on Markowitz Portfolio Optimisation: Plain English — but doing so in the most cost-effective way possible for the UK tax regime. This transforms a tedious, potentially costly chore into a proactive tax optimisation tool. Automated rebalancing is well established among professional managers; this template brings a slice of that discipline to the individual investor.

Regular rebalancing, done efficiently, is vital for long-term success. It systematically enforces the discipline of "selling high" (trimming winners) and "buying low" (adding to laggards), which can enhance returns and reduce volatility over time, improving metrics like the Sharpe Ratio. Don't let tax complexity paralyse you. Use tools like our Portfolio Calculator to track drift and use this free template to execute rebalancing intelligently, keeping your portfolio on track and your tax bill minimised. Explore more Free Tools to support your investment journey.

Why Manual Rebalancing Spreadsheets Still Matter for UK Investors

While institutional wealth managers increasingly automate rebalancing, self-directed UK investors often find spreadsheets indispensable. A well-built spreadsheet offers three compelling advantages for DIY investors: privacy (your data stays offline), flexibility for modelling complex scenarios, and cost accessibility. Unlike subscription-based platforms, a well-built rebalancing spreadsheet costs nothing and adapts to your unique financial life — whether projecting retirement income or stress-testing tax outcomes after a career change.

Manual, unassisted spreadsheets are prone to calculation errors, but this free template mitigates those risks. It automates the mathematically intensive UK tax sequencing that turns routine rebalancing into a tax-optimisation engine. Consider the complexities:

- ISA vs. taxable accounts: Every £20,000 ISA allowance shields future gains from Capital Gains Tax (CGT) and dividends from income tax. The template prioritises moving appreciating assets into this tax-free wrapper first.

- Capital Gains Tax thresholds: With a £3,000 annual exempt amount (2024/25), selling assets in taxable accounts requires precise calculation. Exceed this by £1,000? You’ll pay 18% or 24% on gains — easily avoidable with proactive planning.

- Dividend tax efficiency: Beyond the £500 tax-free dividend allowance, rates jump to 33.75% for higher-rate taxpayers. The template factors this into asset location decisions.

- Stamp Duty Reserve Tax (SDRT): Buying UK shares incurs a flat 0.5% levy — avoidable when purchasing within an ISA. The template sequences trades to minimise this cost.

For example, imagine rebalancing a £100,000 portfolio split between an ISA and taxable account. Manually selling £5,000 of a UK equity fund in a taxable account might trigger CGT, while buying replacement shares could incur SDRT. The template automates "sell in ISA, buy in taxable" sequences to dodge both — potentially saving hundreds annually. It even integrates with Google Sheets' GOOGLEFINANCE function for near-live price updates (typically delayed by around 20 minutes).

Institutional-grade automation can meaningfully reduce rebalancing costs, and this template brings similar rigour to DIY investors. For deeper strategy insights, explore our guide to Markowitz portfolio optimisation or use our portfolio calculator for baseline allocations. While advanced tools exist, spreadsheets remain the Swiss Army knife for UK investors — free, private, and infinitely adaptable.

Why this works for UK investors: ARIA PM’s template encodes HMRC rules directly into its logic, automating what most platforms treat as an afterthought. Test scenarios against your retirement projections or evaluate efficiency using the Sharpe ratio. For more tools, visit our free resources hub.

Step-by-Step: Using the Excel Template for Tax-Smart Rebalancing

1. Input Your Holdings and Targets Start by listing every investment across your accounts — including ISAs, GIAs (General Investment Accounts), and pensions. For each holding, enter:

- Current value

- Original purchase price (for taxable accounts, to track capital gains)

- Asset class (e.g., UK equities, global bonds)

- Target allocation percentage (e.g., 60% equities, 40% bonds)

If you use Microsoft 365, enable the Excel Stocks Data Type to pull live share prices automatically. Google Sheets users can manually update prices via free market data sources.

2. Calculate Portfolio Drift The template instantly compares your current allocations against targets. For example, if your UK equity allocation has risen from 30% to 36% due to market gains, the sheet flags this "drift" and quantifies the adjustment needed. Manual drift calculations in multi-asset portfolios are easy to get wrong — but automation removes that risk.

3. Review Automated Trade Sequences Here’s where tax strategy takes centre stage. The template doesn’t just suggest what to trade — it sequences trades to minimise your UK tax bill:

- Sell losers first in taxable accounts: If a holding in your GIA is below its purchase price, the sheet prioritises selling it to harvest capital losses. These losses offset future tax bills.

- Use your £3,000 CGT allowance strategically: If you must sell winners, the template caps gains within your annual Capital Gains Tax exemption (£3,000 in 2024/25). Gains beyond this face 18% or 24% tax.

- Favour ISA adjustments: Buying or selling within your ISA (£20,000 annual allowance) incurs no CGT or dividend tax. The template routes trades here first, avoiding SDRT (0.5% share purchase tax) and taxable events.

- Minimise unnecessary purchases: To dodge SDRT, the sheet reduces buy orders by first using dividends or sales proceeds from tax-sheltered accounts.

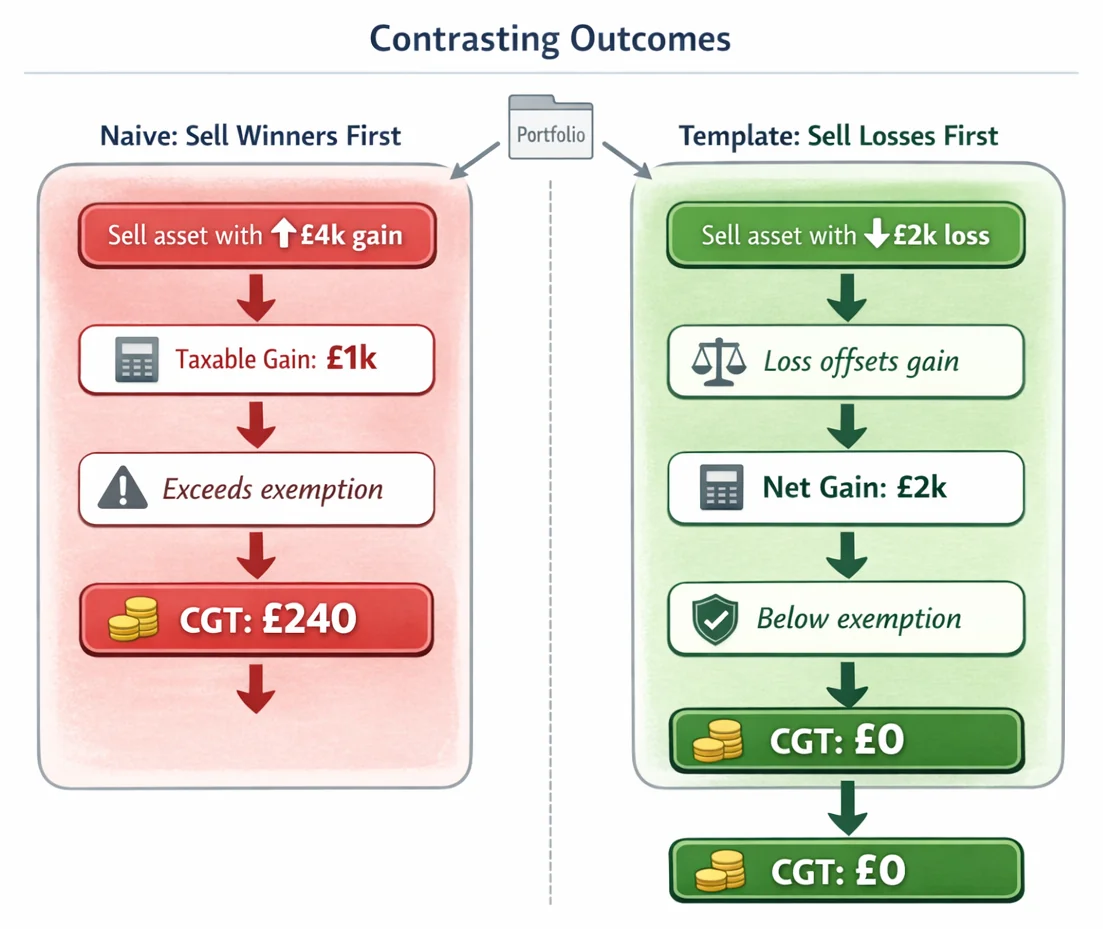

Why This Sequencing Matters Imagine your portfolio needs £5,000 shifted from equities to bonds. A naive approach might sell profitable GIA holdings, triggering CGT. The template instead might:

- Sell a loss-making UK fund in your GIA (harvesting losses).

- Use ISA funds to buy bonds (no tax).

- Only sell GIA winners if essential, keeping gains under £3,000.

This can avoid a needless tax bill — turning rebalancing into a quiet tax-saving tool. For deeper strategy insights, see our guide to Markowitz Portfolio Optimisation: Plain English.

Final Checks Verify trade sizes against your annual ISA allowance and CGT limits. Use our Portfolio Calculator to stress-test scenarios, or explore other Free Tools like our Compound Interest Calculator. Remember: while spreadsheets simplify rebalancing, complex portfolios may benefit from professional tools — especially as finance firms increasingly shift from manual methods.

For ongoing optimisation, bookmark our Sharpe Ratio Explained: A UK Investor's Guide to measure risk-adjusted returns. Ready to start? Download the template via ARIA PM Home.

Real-World UK Examples: How the Template Saves You Tax

For UK investors, the free Excel template transforms routine rebalancing into a strategic tax-optimisation exercise. By automating trade sequencing across taxable and tax-sheltered accounts, it identifies opportunities invisible to manual methods. Consider these scenarios:

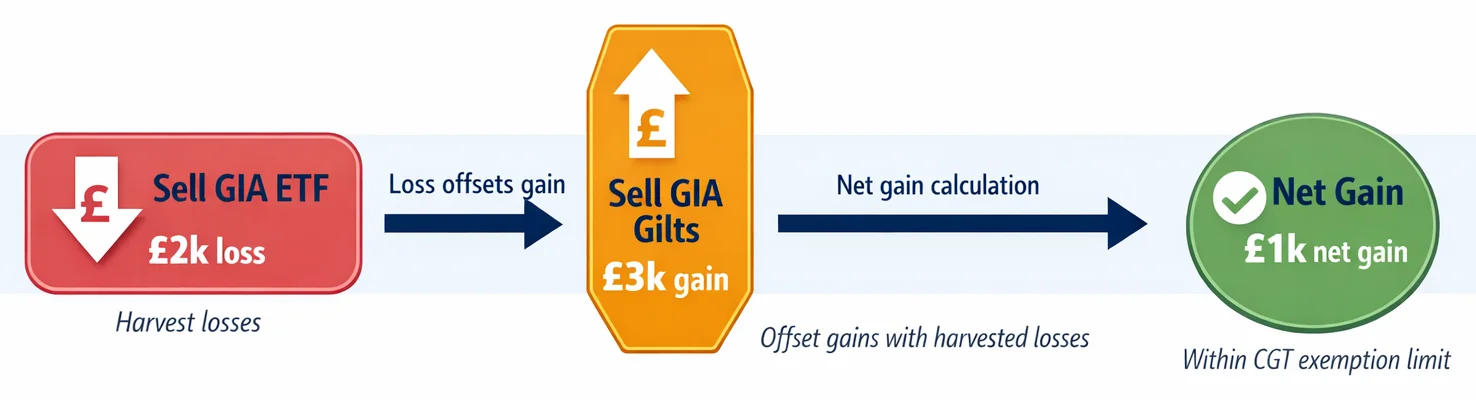

1. The £100k Mixed ISA/GIA Portfolio Imagine your £100,000 portfolio holds 60% global equities (Vanguard FTSE All-World ETF) and 40% UK gilts. Your ISA holds £40,000 of the ETF, while your General Investment Account (GIA) holds the remaining £20,000 ETF and all £40,000 gilts. After a market dip, your GIA-held ETF shows a £2,000 unrealised loss, while gilts have a £4,000 gain.

Without the template:

- You might sell overweight gilts in the GIA, realising a £4,000 gain.

- After using your £3,000 Capital Gains Tax (CGT) annual exempt amount, you owe 18% CGT on the remaining £1,000.

- But the £2,000 ETF loss goes unused.

With the template:

- It prioritises selling the loss-making ETF in the GIA first.

- The £2,000 loss offsets part of the gilt gain, leaving only £2,000 taxable gain.

- After the £3,000 exemption, CGT owed: £0.

- Savings: £180 (18% of the £1,000 that would otherwise be taxed) plus avoided Stamp Duty Reserve Tax (SDRT) on replacement purchases (0.5% on share buys).

2. Platform Integration: The Interactive Investor Workflow The template syncs with broker exports (e.g., Interactive Investor CSV files). Suppose your annual rebalance requires shifting £5,000 into a UK equity holding. Manually, you might:

- Sell assets in your GIA, triggering CGT on any realised gain.

- Buy UK shares, incurring 0.5% SDRT (£25 on a £5,000 purchase).

The template analyses your holdings across accounts and directs trades into your ISA first (using its £20,000 annual allowance). By buying the UK shares inside the ISA and rebalancing there, you dodge both CGT and SDRT. For GIA-heavy investors, this can avoid meaningful sums in transaction taxes each year.

3. Dividend Drift: The Silent Portfolio Killer Your GIA’s quarterly dividend reinvestment gradually skews allocations. Manually correcting this might involve selling appreciated assets, realising gains. The template helps you avoid that by:

- Calculating "drift tolerance" thresholds.

- Using dividend cash to buy underweight assets (e.g., topping up bonds with £500 dividends) instead of forcing a sale.

- Only selling as a last resort, minimising CGT events.

Dividends received in a GIA are taxable above the £500 allowance — at 8.75% (basic), 33.75% (higher) or 39.35% (additional rate). A basic-rate investor with £10,000 of GIA dividends pays 8.75% on the £9,500 above the allowance, roughly £831 in dividend tax. Holding income-producing assets inside an ISA instead removes that tax entirely, and the template flags where dividend cash can do the rebalancing work that would otherwise require a taxable trade.

The Efficiency Multiplier Professional managers increasingly automate portfolio analytics precisely because manual processes waste time and introduce errors. For retail investors, automating trade sequencing cuts both errors and time, and can meaningfully reduce trading costs. By turning rebalancing into a tax-aware engine, the template compounds savings: a £100,000 portfolio avoiding £500/year in unnecessary taxes, with that £500 reinvested each year, grows to roughly £6,900 more over 10 years (at 7% returns) than an unoptimised one.

For deeper strategy, see our guide on Markowitz Portfolio Optimisation or test scenarios with our Portfolio Calculator. Explore all Free Tools to maximise your tax efficiency.

5 Costly Rebalancing Mistakes (and How the Template Fixes Them)

Rebalancing isn't just about percentages — it's a tax minefield for UK investors. Manual approaches often trigger avoidable bills or miss savings. Here’s how common errors erode returns, and how our free Excel template uses automated tax-logic to prevent them:

Triggering Unnecessary CGT by Selling Winners First: Selling appreciated assets in your General Investment Account (GIA) first can create an immediate Capital Gains Tax bill. Gains above your £3,000 annual exempt amount are taxed at 18% or 24%. Many investors liquidate winners instinctively, wasting their allowance on gains that could have been deferred. Template Fix: The tool sequences trades intelligently. It prioritises selling loss-making assets in your GIA first. Realised losses offset any unavoidable gains, minimising your current tax bill. Winners are only sold if essential, and ideally held longer to potentially benefit from lower future rates or allowances.

Ignoring Tax-Wrapper Differences: Treating ISAs and GIAs the same is a costly error. Selling assets within an ISA is tax-free, while selling in a GIA can trigger CGT. Also, dividends in a GIA are taxable (after the £500 allowance), unlike in an ISA. Manual rebalancing often overlooks this, leading to unnecessary GIA transactions. Template Fix: The spreadsheet separates holdings by tax wrapper. Its engine prioritises rebalancing trades within your ISA first, where transactions are tax-neutral. It only suggests GIA trades when absolutely necessary, and sequences them to be tax-efficient (as above). This protects your valuable ISA allowance for future contributions.

Manual Calculation Errors: Calculating target trades across multiple accounts and asset classes manually is complex. Errors like misallocating funds, miscalculating percentages, or overlooking fees are common, leading to over/under-trading, unintended risk exposure, or tax inefficiency. Template Fix: Automation eliminates guesswork. Input your holdings and target allocations once. The template instantly calculates the precise buys and sells needed across all accounts to hit your targets, factoring in current values and minimising unnecessary trades. This reduces error risk and saves time. For deeper analysis, pair it with our Portfolio Calculator.

Infrequent Rebalancing: Many investors never rebalance to a set schedule. Letting your portfolio drift significantly increases risk — your actual allocation may no longer match your intended strategy, potentially exposing you to more volatility than you can stomach. It also defers tax-saving opportunities like loss harvesting. Template Fix: The template visually flags drift. It compares your actual holdings against your target allocations, clearly highlighting which assets are over or underweight. This constant visibility acts as a prompt, encouraging timely rebalancing to maintain your desired risk level — a core principle of Markowitz Portfolio Optimisation: Plain English.

Overlooking Loss Harvesting: Failing to strategically realise losses in your GIA wastes a valuable tax tool. These losses can be used to offset capital gains in the same year or carried forward indefinitely. Many investors forget to check for loss-making assets when rebalancing, missing this chance to reduce their tax liability. Template Fix: The template’s tax engine actively scans your GIA holdings. It identifies assets currently sitting at a loss relative to their purchase price. During rebalancing calculations, it prioritises selling these "loss-makers" where appropriate, automatically realising losses that can be used to shelter gains elsewhere, effectively turning routine maintenance into a tax-saving exercise. Explore more Free Tools to enhance your strategy.

By automating the UK-specific tax logic behind trade sequencing decisions, this free spreadsheet transforms rebalancing from a mathematical chore into a systematic engine for tax efficiency. It ensures your portfolio maintenance actively works to preserve more of your hard-earned returns. For understanding how this impacts your risk-adjusted performance, see Sharpe Ratio Explained: A UK Investor's Guide.

Your Next Steps: Implementing the Template for Maximum Tax Efficiency

Ready to transform routine rebalancing into a tax-optimisation tool? Follow these four UK-specific steps to activate your free Excel template’s hidden potential. First, download the template directly from our resource library. This isn’t just another spreadsheet — it’s engineered to automate the complex sequencing of trades across taxable and tax-sheltered accounts, a critical edge for UK investors.

Next, input your current holdings and target allocations. Crucially, include every investment in both your ISA (tax-free wrapper) and General Investment Account (GIA). Why? The template cross-analyses these to prioritise tax-efficient actions. For example:

- Selling assets in your GIA could trigger Capital Gains Tax (CGT) if gains exceed your £3,000 annual exemption.

- Purchasing UK shares incurs 0.5% Stamp Duty Reserve Tax (SDRT) — a flat 0.5% rate that adds up with frequent trades.

- Dividends in a GIA face taxation above your £500 allowance (8.75%-39.35%), while ISAs shelter them entirely. The template’s algorithm weighs these rules, suggesting moves like "sell bond funds in GIA first (lower growth potential, minimising CGT) before touching equity ETFs" or "maximise UK stock purchases within your ISA to dodge SDRT."

Third, set quarterly or semi-annual review reminders. Consistency prevents portfolio drift — imagine your 60% equity allocation creeping to 70% after a market rally, exposing you to unnecessary risk. Regular check-ins let you correct course while using annual allowances. Use our Portfolio Calculator to model adjustments stress-free.

Finally, always run the template’s sequence check before executing trades. This step is non-negotiable. It calculates whether rebalancing through your ISA first (using your £20,000 annual allowance) or harvesting GIA losses offsets gains more efficiently. One misstep — like selling a high-gain asset in your GIA when your CGT exemption is exhausted — could cost hundreds in avoidable taxes.

You might wonder: with so much professional software available, why start with a spreadsheet? Precisely because DIY investors need simplicity. Complex software often overcomplicates basic rebalancing, while this template distils tax logic into a clear, customised plan. With recent overhauls like the Financial Services and Markets Act 2023 empowering the FCA to heighten consumer protections, taking control of your tax efficiency aligns perfectly with regulatory shifts toward transparency.

Consistency transforms this tool into your personal tax-efficiency engine. Each quarterly review compounds savings — a one-off £200 in avoided SDRT or optimised CGT, reinvested and left to grow at 5% annual returns, becomes roughly £530 over 20 years. For deeper analysis (like stress-testing allocations against UK tax reforms), tools like ARIA PM automate survivorship bias adjustments and regime modelling. But for most investors, this template — paired with resources like our Sharpe Ratio Guide or Markowitz Optimisation Primer — is the simplest path to keeping more of your profits.

Start today. Your portfolio’s efficiency is just a spreadsheet away.

Key Takeaways

- This free Excel template automates UK tax-efficient trade sequencing during rebalancing, turning routine maintenance into a significant Capital Gains Tax (CGT) and Stamp Duty Reserve Tax (SDRT) minimisation tool.

- The template strategically sequences trades to maximise the use of your annual £3,000 CGT exempt allowance before triggering taxable gains.

- It minimises unnecessary SDRT by prioritising purchases within tax wrappers like ISAs and avoiding new UK share purchases where possible.

- The tool prevents naive selling of winners by calculating trades that minimise realised gains while still achieving your target asset allocation.

- Automating this complex tax logic overcomes the primary hurdle preventing many UK investors from rebalancing regularly.

| Feature | Manual Rebalancing | Free Excel Template |

|---|---|---|

| Tax-Efficient Sequencing | Complex to calculate; often overlooked | Automated prioritisation of tax-sheltered accounts |

| Account-Specific Rules | Prone to ISA/GIA/pension confusion | Applies correct tax logic per account type |

| Loss Harvesting | Difficult to spot opportunities | Auto-identifies loss offsets in GIAs |

| CGT Minimisation | Risk of triggering gains in GIAs | Sells winners in ISAs/pensions first |

| Time Required | Hours of calculations & cross-checks | Generates trade list in <5 minutes |

| Privacy | Maintained (local spreadsheet) | Maintained (local Excel file) |

5 Costly Rebalancing Mistakes and Template Solutions

| Mistake | Cost Implication | How Template Fixes It |

|---|---|---|

| Selling winners in GIAs first | Unnecessary Capital Gains Tax | Sequences ISA/pension trades before GIAs |

| Overlooking loss-harvesting chances | Missed tax offsets against future gains | Flags underwater GIA positions automatically |

| Ignoring dividend cash during rebalance | Inefficient cash deployment | Factors dividends into allocation maths |

| Manual calculation errors | Allocation drift & tax inefficiencies | Automated % calculations with live updates |

| Treating accounts separately | Suboptimal cross-account tax outcomes | Holistic view of ISA/GIA/pension interactions |

Sources

- FCA: InvestSmart — FCA's consumer investing hub covering diversification, risk management, and portfolio maintenance principles for UK investors.

- SEC: Rebalancing Your Portfolio — SEC investor bulletin explaining rebalancing mechanics, benefits, and strategic considerations.

- MoneyHelper: Investing — UK government-backed guidance on investing, asset allocation, and managing your portfolio.

- Vanguard UK: Principles for investing success — Vanguard's framework for disciplined investing, including rebalancing strategies and cost efficiency.

- Microsoft Support: Excel help & learning — Official documentation for Excel's financial tools and template customisation options.

- CFA Institute: Portfolio Rebalancing — Science and Techniques — Practitioner research summary on evidence-based rebalancing methodologies and thresholds.